المحتويات

مقال

How the tech sell-off could shape the next move in US indices

February 4, 2026

مقال

How the tech sell-off could shape the next move in US indices

February 4, 2026

مقال

How the tech sell-off could shape the next move in US indices

February 4, 2026

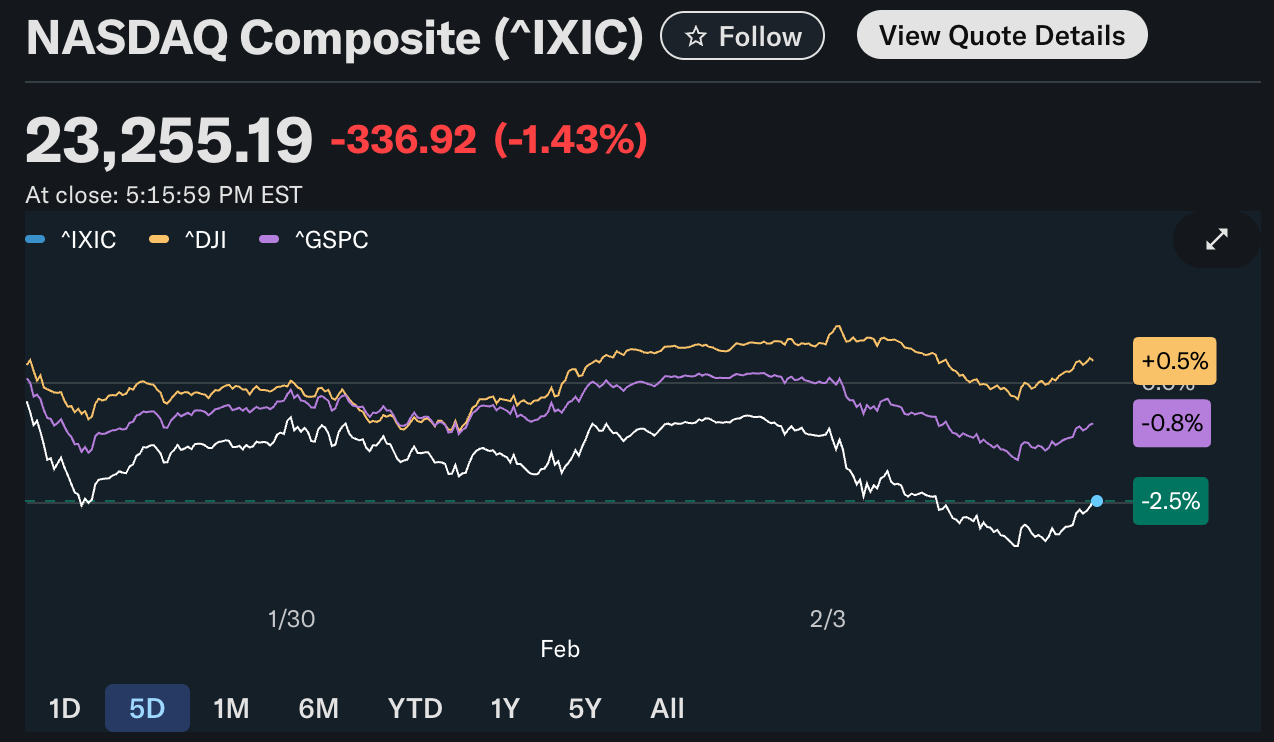

The latest bout of selling in technology stocks suggests US equity indices are entering a more delicate phase, where market leadership is being tested rather than assumed. On Tuesday, the Nasdaq Composite slid 1.4%, pulling the S&P 500 lower by 0.8%, as investors reassessed whether the AI-led rally still supports current valuations.

Rather than signalling an outright trend break, the move points to a market adjusting expectations. With earnings scrutiny intensifying and volatility beginning to spill into other asset classes, the next direction for US indices will hinge on whether large technology firms can reassert confidence or whether rotation away from concentrated growth exposure continues.

What’s driving the tech sell-off?

The immediate pressure stemmed from renewed concerns over the sustainability of AI-related spending. Although Palantir’s earnings supported the longer-term AI narrative, they failed to ease worries about rising costs and diminishing returns across the sector. Nvidia’s near-3% decline weighed heavily on sentiment after reports suggested cooling ties with OpenAI, raising questions about demand visibility for its latest generation of AI chips.

That unease spread quickly through the software and cloud space. Shares in Amazon and Microsoft extended their recent pullbacks as investors reduced exposure to richly valued names. Meanwhile, Anthropic’s launch of a legal productivity tool reinforced fears that rapid innovation could intensify competition and compress margins. Markets are no longer rewarding AI exposure by default; they are increasingly focused on execution and profitability.

Why it matters for US Indices

US equity indices have grown more dependent on a narrow group of mega-cap technology stocks. The largest technology companies now account for more than 30% of the S&P 500’s total market value, leaving benchmarks vulnerable when sentiment shifts against the sector. When leadership weakens, index stability can erode quickly.

As one US equity strategist put it, “The question isn’t whether AI will transform industries, but whether earnings can justify the expectations already priced in.” That gap between narrative and delivery explains why markets can decline even during strong reporting periods. For indices, the greater risk is not a sharp collapse, but an extended stretch of uneven performance and sector rotation.

Impact on markets and investors

The sell-off has already altered market positioning. While equities moved lower, investors shifted towards defensive assets, driving gold higher by more than 6% in a single session - its strongest daily gain since 2008 - following its sharpest one-day drop in over four decades just days earlier. Silver also rebounded sharply, rising around 9% as buyers stepped in aggressively.

This divergence suggests investors are trimming momentum exposure rather than exiting risk altogether. Weakness in equities alongside strength in precious metals points to hedging behaviour rather than panic selling. For traders, it signals a market environment where price action may become more two-sided, with rallies meeting resistance sooner and dips attracting more selective interest.

Expert outlook

The next move for US indices will be influenced by upcoming earnings from AMD, Amazon, and Alphabet, which should offer clearer insight into AI spending trends, margin pressures, and demand durability. AMD’s results are being closely watched as an indicator of whether increased competition in AI hardware can support broader growth without eroding profitability.

Most strategists remain cautious rather than overtly bearish. Expectations are building for higher volatility as markets shift from optimism driven by long-term narratives to scrutiny grounded in earnings delivery. If Big Tech can demonstrate both growth and cost discipline, indices may find stability. If not, US equities could drift into a broader consolidation phase, defined by rotation rather than sustained gains.

Key takeaway

The tech sell-off reflects a recalibration in how growth is priced, rather than a rejection of the AI theme itself. US indices remain underpinned, but leadership is increasingly conditional on earnings credibility. The sharp move into gold highlights growing caution beneath the surface. The next phase for markets will depend on whether Big Tech can continue to justify its outsized influence on index performance.

إخلاء مسؤولية:

The information contained on the Deriv Market News is for educational purposes only and is not intended as financial or investment advice. The information may become outdated, and some products or platforms mentioned may no longer be offered. We recommend you do your own research before making any trading decisions. The performance figures quoted refer to the past, and past performance is not a guarantee of future performance or a reliable guide to future performance.

الأسئلة الشائعة

Why did US indices fall even after strong AI earnings?

Does the Nasdaq’s decline signal a broader market downturn?

Why did gold rise as stocks fell?

Are fears of an AI bubble increasing?