المحتويات

مقال

Oil outlook: Why geopolitics still isn’t lifting crude

January 5, 2026

مقال

Oil outlook: Why geopolitics still isn’t lifting crude

January 5, 2026

مقال

Oil outlook: Why geopolitics still isn’t lifting crude

January 5, 2026

.png)

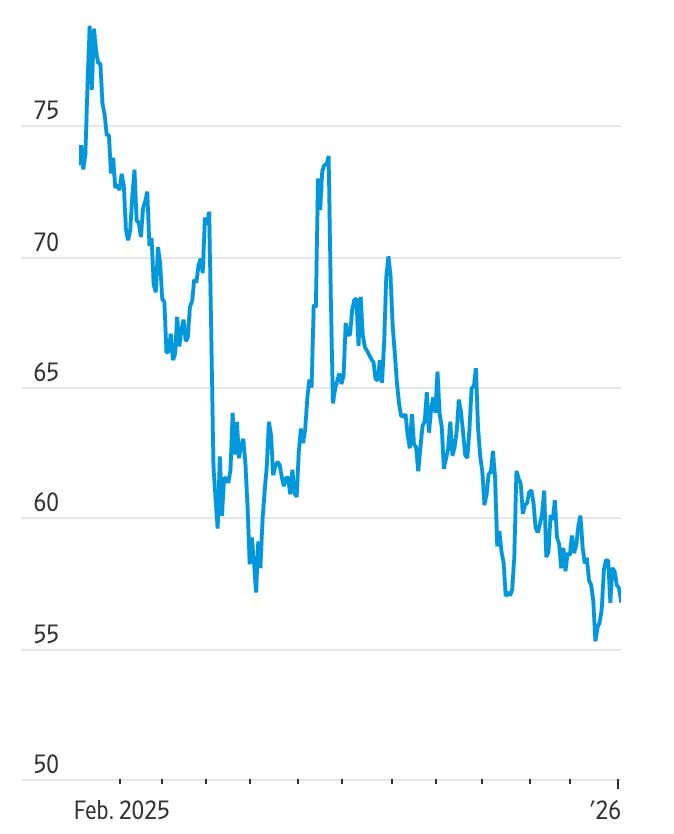

Geopolitical turmoil once acted as a reliable catalyst for oil rallies, but analysts argue that its influence has faded. Even after the removal of Venezuela’s President Nicolás Maduro and President Donald Trump’s promise to reopen the country to US oil companies, crude markets remained largely unmoved. US oil traded near $57 a barrel, while Brent hovered just above $60, both close to multi-year lows.

According to analysts, the muted reaction reflects deeper structural forces at play. Global supply remains ample, demand growth is slowing, and alternative producers retain enough spare capacity to cushion shocks. Until those dynamics shift, geopolitical events may dominate headlines without delivering lasting support for oil prices.

What’s driving oil prices?

Oversupply continues to shape the direction of the oil market. OPEC+ has opted to maintain steady production, while output from non-OPEC producers, particularly the United States, remains elevated. That imbalance has weighed heavily on prices, with US crude declining by roughly 20% last year, highlighting how supply resilience has outpaced demand.

Venezuela’s political transition adds complexity but little immediate relief. Current production sits between 800,000 and 1.1 million barrels per day, far below the 3.5 million barrels per day seen in the late 1990s. Even under favourable conditions, rebuilding output would require sustained investment and political stability, making any material supply increase a long-term rather than near-term development.

Why it matters

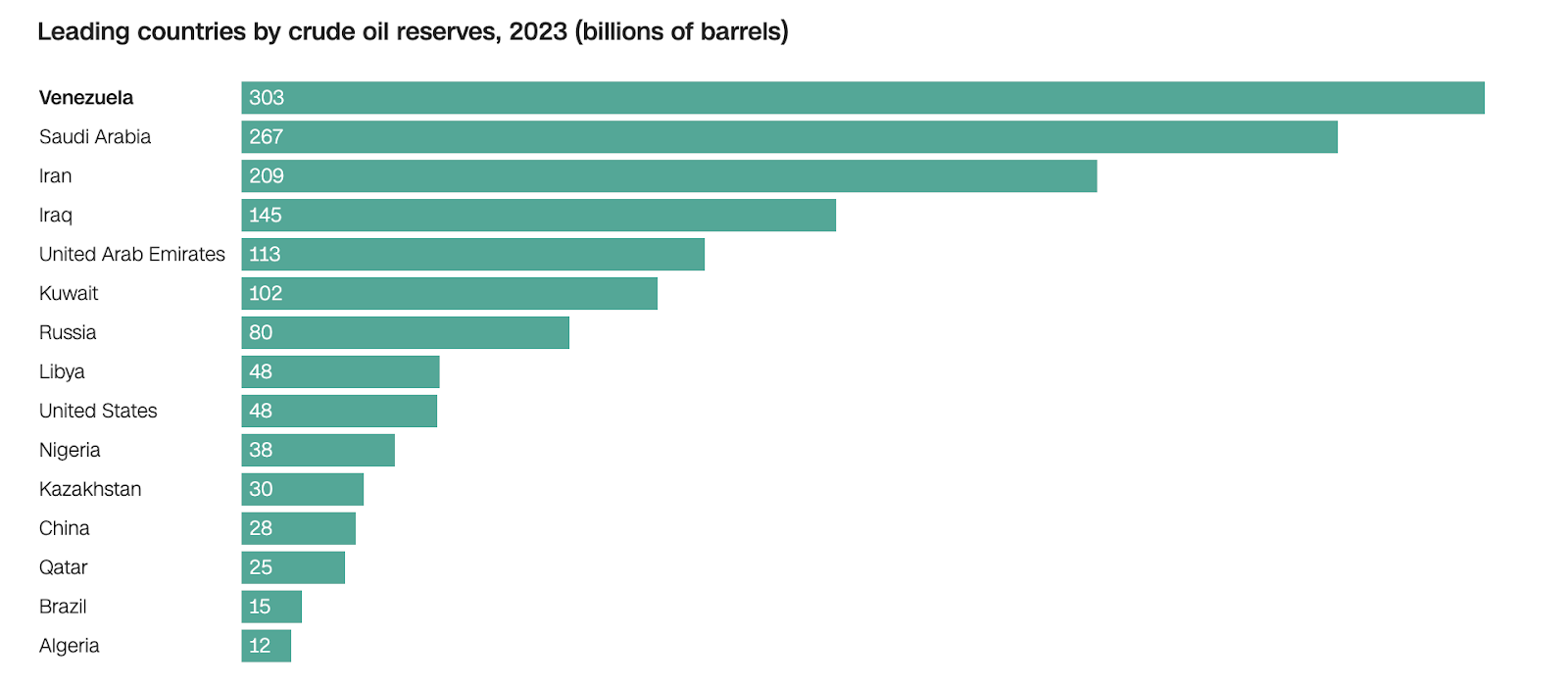

For market participants, immediacy matters more than potential. Oil prices respond to barrels that can be delivered today, not reserves that may take years to unlock. Although Venezuela holds the world’s largest proven crude reserves at 303 billion barrels, those reserves remain effectively constrained by ageing infrastructure, sanctions, and ongoing political risk.

Goldman Sachs’ head of oil research, Daan Struyven, has described the fallout from Maduro’s removal as uncertain in the short run. While sanctions relief could eventually support higher production, the risk of temporary disruptions remains. In the meantime, excess supply continues to dominate price formation, limiting the market’s sensitivity to geopolitical shifts.

Impact on the Oil market

The net effect is a cap on prices rather than a boost. Analysts estimate that even with full sanctions relief, Venezuela might add only several hundred thousand barrels per day within the first year, assuming a smooth transition of power. In a market already oversupplied, that increase would likely be absorbed without much difficulty.

This helps explain why Brent briefly slipped below $61 before stabilising and why volatility has remained relatively contained. As Capital Economics has pointed out, spare capacity elsewhere allows the market to absorb regional disruptions, particularly while OPEC+ shows little appetite for aggressive supply cuts amid uncertain demand growth.

Expert outlook

Looking further ahead, analysts broadly expect oil prices to remain range-bound, with risks skewed to the downside. Capital Economics projects crude drifting towards $50 a barrel over the coming year as global supply growth continues to exceed demand. Any successful recovery in Venezuelan output would likely reinforce that trend rather than reverse it.

The main uncertainty lies in execution. Industry estimates suggest it would take around $10 billion per year to restore Venezuela’s oil sector, and that level of investment depends on long-term political stability. Until credible reforms and durable sanctions relief emerge, Venezuelan oil remains a future consideration in a market focused firmly on near-term balance.

Key takeaway

Geopolitical events no longer guarantee higher oil prices. With supply plentiful and Venezuela’s production recovery still years away, fundamentals continue to limit crude’s upside. Unless demand strengthens materially or producers move to tighten supply, analysts expect oil to stay under pressure. Monitoring sanctions developments, OPEC policy decisions, and US output trends will be key to identifying the next meaningful shift.

Oil technical outlook

US oil remains under short-term pressure, struggling to regain momentum above the 57.47–58.40 resistance zone, which keeps the broader bias tilted lower. Recent stabilisation attempts have been met with fresh selling, leaving price hovering just above the 56.40 area, while 55.37 stands out as a key support level.

Momentum signals support this cautious view. The RSI has slipped below its midpoint, indicating a decline in bullish momentum, while price action remains capped below key resistance. Bollinger Bands indicate elevated volatility, though without a clear directional break.

A sustained move below 55.37 could trigger deeper, liquidation-driven selling. Conversely, any meaningful recovery would require a decisive break back above 58.40 to shift the short-term outlook.

إخلاء مسؤولية:

The performance figures quoted refer to the past, and past performance is not a guarantee of future performance or a reliable guide to future performance.

الأسئلة الشائعة

Why didn’t oil prices rise after Venezuela’s political upheaval?

How much oil does Venezuela produce today?

Can US oil companies quickly revive Venezuelan production?

Does Venezuela’s return threaten OPEC strategy?

What is the biggest risk for oil prices now?