المحتويات

مقال

Silver tightens as Copper falters: Is a supply-led metals rally taking hold?

February 10, 2026

مقال

Silver tightens as Copper falters: Is a supply-led metals rally taking hold?

February 10, 2026

مقال

Silver tightens as Copper falters: Is a supply-led metals rally taking hold?

February 10, 2026

The balance of evidence suggests a supply-led phase is emerging across key metals markets. Silver inventories have fallen to levels last seen nearly a decade ago, while copper output from Chile, the world’s largest producer, continues to decline even as prices remain elevated. This is not a short-lived demand spike. It reflects tightening physical conditions.

When higher prices coincide with shrinking stockpiles and weakening production, markets are forced to reprice fundamentals rather than sentiment. Silver and copper are increasingly shaped by availability constraints, with physical supply exerting greater influence than speculative positioning in setting near- and medium-term direction.

What’s driving the tightness in Silver and Copper?

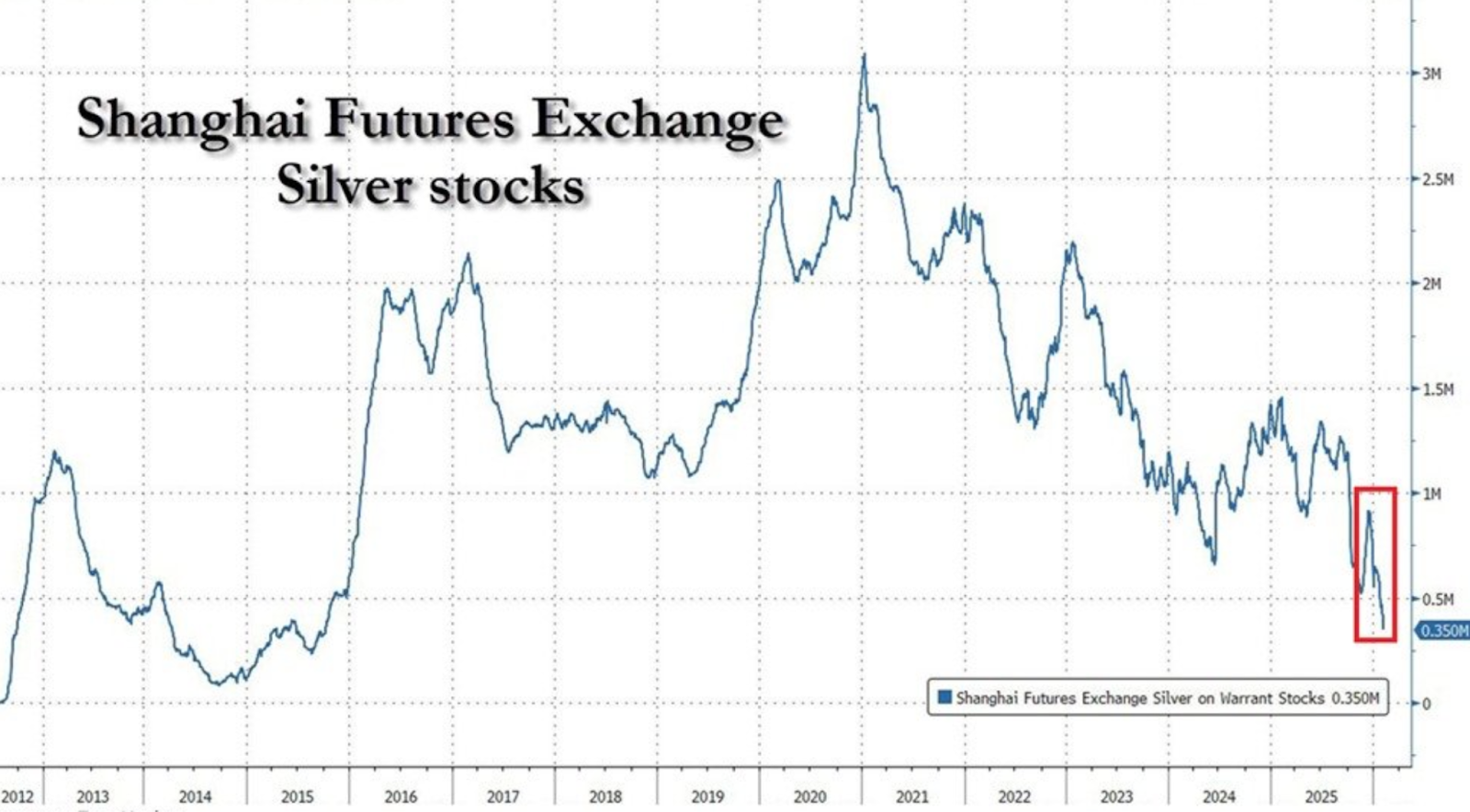

Silver’s tightening backdrop is rooted in declining physical inventories. Deliverable stocks on the Shanghai Futures Exchange have fallen to roughly 350 tonnes, the lowest level since 2015 and an 88% decline from the 2021 peak.

This steady erosion reflects sustained industrial demand, limited expansion in mine supply, and significant export flows. During 2025, large volumes of silver were shipped from China to London, easing pressure in global hubs while further draining domestic reserves. The net effect has been a local market with little buffer against demand shocks.

Price behaviour is increasingly mirroring that fragility. Even as XAG/USD slipped towards $82.50 amid profit-taking and a modest US Dollar rebound, downside momentum remained contained. Traders appear hesitant to force deeper corrections in a market where physical availability is already stretched. Supply conditions are now acting as an anchor beneath price action.

Copper’s constraint is less visible but more structural. Chile’s copper exports rose 7.9% year-on-year in January to $4.55 billion, yet the increase was driven almost entirely by a 34% rise in prices, not stronger volumes. Output has declined year-on-year for five consecutive months, reflecting the cumulative impact of ageing mines, declining ore quality, labour disruptions, and operational bottlenecks.

Why it matters

When elevated prices fail to trigger a production response, long-held assumptions begin to fray. Analysts at Bloomberg Intelligence have noted that Chile’s difficulties highlight a wider industry challenge: new copper supply is becoming harder to access, slower to develop, and increasingly exposed to technical and political risk. Price alone is no longer a reliable solution.

Silver faces a similar constraint from a different angle. Much of its supply is tied to by-product production, limiting flexibility when prices rise. As one London-based metals strategist observed, silver often appears plentiful on paper but scarce in practice. In such conditions, relatively small shifts in demand can translate into disproportionate price moves.

Impact on markets, industry, and inflation

For markets, this points to a change in character. Rallies driven by supply stress tend to be more durable than those fuelled by cyclical demand. Silver remains sensitive to US macroeconomic releases, but each pullback increasingly encounters depleted inventories. That dynamic encourages buying on weakness rather than chasing momentum.

For the industry, particularly in renewables and electrification, the implications are more tangible. Silver remains essential for solar manufacturing, while copper is foundational to power infrastructure and electric vehicles. Persistent tightness raises costs, complicates procurement strategies, and feeds into longer-term pricing pressures.

For policymakers, the environment is less forgiving. Even if growth moderates, constrained metals supply can sustain inflationary forces. This challenges disinflation narratives and reinforces the role of commodities as a structural hedge rather than a purely cyclical trade.

Expert outlook

Silver’s near-term trajectory is likely to remain closely tied to US economic data, including Retail Sales and delayed labour market releases. Evidence of slowing growth or easing inflation would typically support prices, particularly given silver’s defensive appeal amid ongoing geopolitical uncertainty in the Middle East.

Copper’s outlook unfolds on a longer timeline. Industry consensus suggests Chile’s production challenges will not be resolved quickly. New projects face environmental, technical, and regulatory hurdles, while existing mines grapple with declining grades. Even if prices pause, the lack of spare capacity points to an extended period of structural tightness.

Silver technical outlook

Silver has stabilised following a sharp pullback from recent highs, with price consolidating near the centre of its recent range after an extended advance. Bollinger Bands remain widely expanded, signalling that volatility is still elevated despite the recent cooling in price action.

Momentum indicators reflect a pause rather than a reversal. The RSI has flattened around the midline after retreating from overbought levels, indicating neutral momentum following earlier extremes.

Trend strength remains pronounced, with elevated ADX readings suggesting the broader trend structure is intact even as short-term momentum eases. Price continues to trade well above prior consolidation zones around $57 and $46.93, underscoring the scale of the preceding move.

Key takeaway

Silver and copper are increasingly shaped by supply realities rather than sentiment alone. Collapsing inventories and faltering production point to a market environment where scarcity defines the downside. Silver’s physical tightness and copper’s structural constraints suggest upside risks remain skewed higher, even amid macro uncertainty. The decisive question is no longer demand strength, but whether supply can meaningfully recover at all.

إخلاء مسؤولية:

The information contained on the Deriv Market News is for educational purposes only and is not intended as financial or investment advice. The information may become outdated, and some products or platforms mentioned may no longer be offered. We recommend you do your own research before making any trading decisions.

الأسئلة الشائعة

Are silver prices rising because of demand or supply?

Why haven’t high copper prices boosted output in Chile?

Can a stronger US Dollar derail silver’s rally?

Does this signal a broader commodities rally?

What should traders watch next?