Contents

Article

Oil market outlook: Will record hedge fund shorts drive WTI toward $55?

October 28, 2025

Article

Oil market outlook: Will record hedge fund shorts drive WTI toward $55?

October 28, 2025

Article

Oil market outlook: Will record hedge fund shorts drive WTI toward $55?

October 28, 2025

According to market analysts, WTI crude could approach the $55 per barrel mark as hedge funds ramp up record short positions amid persistent oversupply and weakening demand signals.

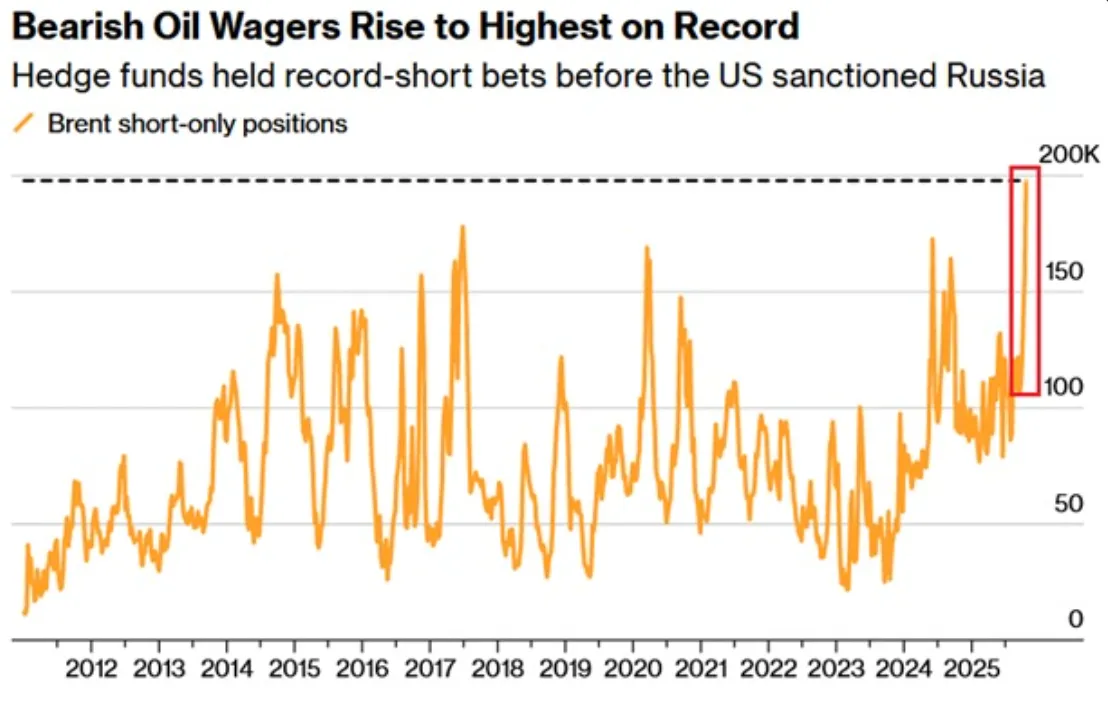

Short calls on Brent jumped by 40,233 contracts in the week ending 21 October, bringing total bearish positions to 197,868 - the highest ever recorded. This marks the third straight week of increased bearish activity and a doubling of short exposure over the past three months. The trend reflects growing conviction among institutional traders that production is expanding faster than consumption, with OPEC+ adding more barrels and global demand remaining sluggish.

Still, fresh U.S. sanctions on Russian oil and shifting OPEC production plans continue to inject volatility. Short-covering rallies toward $65 per barrel can’t be ruled out as macro fundamentals and geopolitics pull prices in opposite directions.

Key takeaways

- Record hedge-fund shorts: Bearish bets on Brent and WTI have doubled since July, highlighting institutional caution.

- Short-term volatility: U.S. sanctions on Russia briefly lifted Brent prices by 10%, though momentum faded quickly.

- Bearish fundamentals: Rising output from OPEC+ and record U.S. production continue to weigh on sentiment.

- Structural shift: Rising U.S. shale production costs could limit downside in the longer term.

- Price risk: If oversupply persists, WTI could test $55, but a short-covering move back toward $65 remains possible.

Hedge fund oil trading takes control of the narrative

Speculative funds have become increasingly bearish. In the week ending 21 October, short positions in Brent futures jumped by more than 40,000 contracts, marking the largest weekly increase since records began.

This surge signals growing confidence that weak demand and excess supply will pressure prices lower. A year earlier, total short positions stood at only 26,000 contracts. The shift mirrors the patterns seen in 2018 and 2020, when a mix of high inventories and a strong U.S. dollar triggered broad oil market corrections.

OPEC oil production increase is overwhelming the market

Oil’s rebound last week - an 8% rally following Washington’s sanctions on Russia’s Rosneft and Lukoil - proved short-lived.

Within days, prices pulled back as OPEC+ members signalled another output increase in November, estimated at around 137,000 barrels per day. Saudi Arabia, leading the initiative, aims to regain market share even if it means accepting lower prices in the near term.

This strategy, combined with rising production from the U.S., Brazil, and Canada, has created an environment of sustained oversupply. Despite geopolitical risks, traders remain more focused on the supply surge that continues to cap prices.

Demand weakness compounds the pressure

Analysts at Standard Chartered have trimmed their 2026–2027 oil price forecasts by $15 per barrel, citing a shift to contango - where future prices trade above spot levels, indicating short-term softness.

The International Energy Agency (IEA) and S&P Global share similar views, both expecting crude to dip below $60 early next year as sluggish demand and trade uncertainty persist.

Even record refinery activity, now exceeding 85 million barrels per day, has not been enough to absorb the surplus. With global consumption underperforming expectations, inventories are likely to build further into 2026.

Geopolitical shocks can still spark short-covering rallies

The bearish setup isn’t immune to sudden reversals. Sanctions imposed by the Trump administration on Russia’s oil sector recently pushed prices up 10% within a week, demonstrating how quickly sentiment can shift.

Potential disruptions involving Ukraine, Iran, or renewed U.S.–China trade tensions could trigger short-covering rallies that briefly lift WTI above $65. However, most analysts agree such reactions would likely be temporary, as the broader supply picture and rising U.S. output continue to dominate the market narrative.

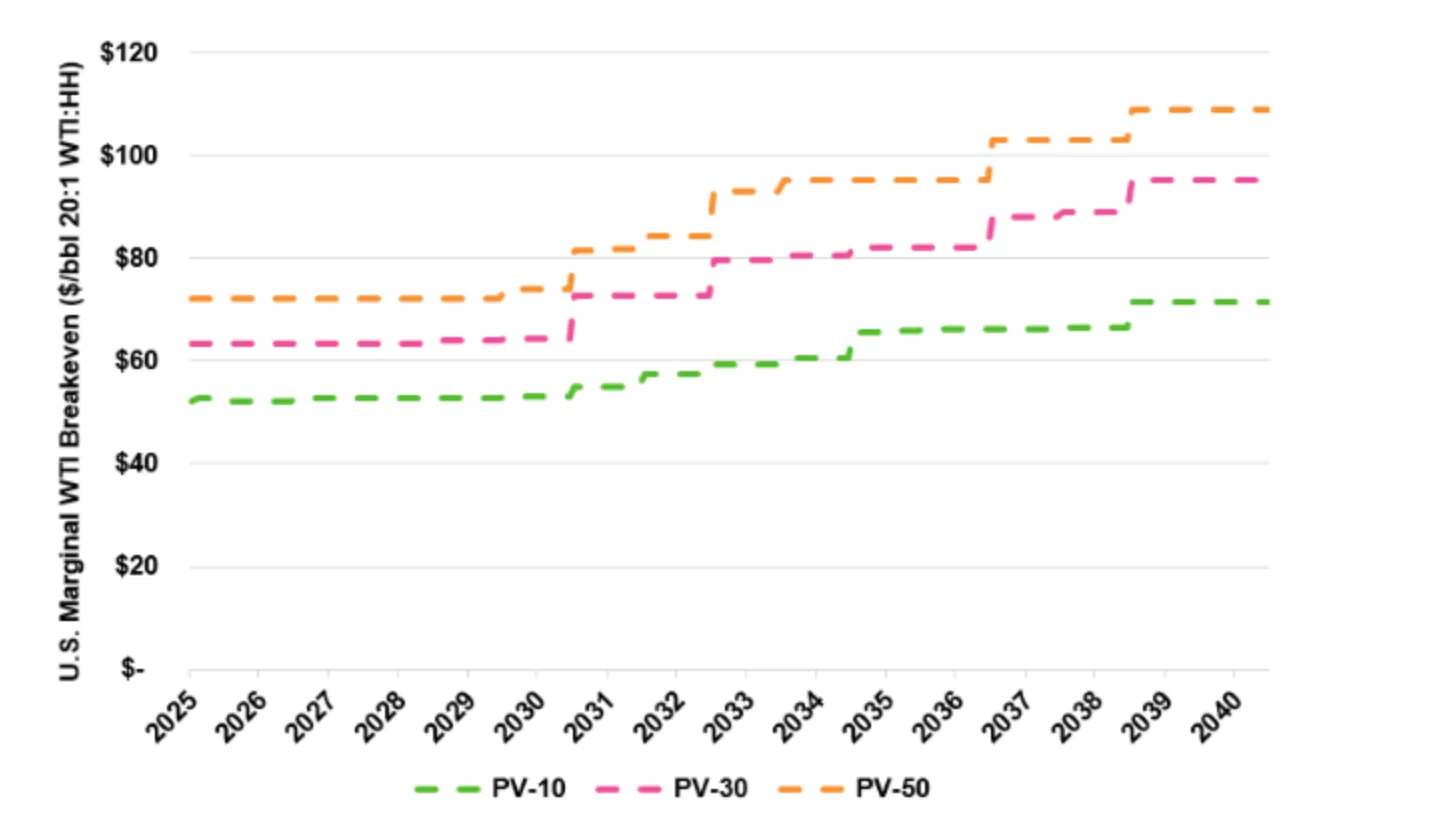

The structural story: rising shale costs and long-term tightness

While near-term conditions favour lower prices, the cost of U.S. shale production is steadily climbing. According to Enverus, marginal costs could increase from $70 to $95 per barrel by the mid-2030s as producers move beyond the most productive wells.

This structural shift could eventually reduce supply if prices fall too low, paving the way for tighter markets once demand steadies. For now, however, shale efficiency gains are keeping output robust despite the challenging price environment.

Oil price market impact and price scenarios

If the current oversupply trend persists, analysts see Brent stabilising near $60 and WTI hovering around $55 by early 2026.

A change in sentiment - such as large-scale short-covering or renewed sanctions risk - could spark short-lived recoveries toward $65–$70. At present, however, the market bias remains tilted lower as supply growth outpaces demand recovery.

Many traders monitor these price levels using Deriv’s trading calculator, which helps evaluate position size, margin, and exposure under different volatility conditions.

Oil technical insights

Oil prices are consolidating near the upper Bollinger Band on Deriv MT5, following a rebound from recent lows - a signal of slowing bearish pressure.

The RSI continues to climb modestly around the midline, suggesting neutral momentum.

Resistance levels remain near 62.35 and 65.00, while 56.85 acts as the key support threshold. A break below that level could invite additional selling pressure, while consolidation above $60 may keep prices range-bound for now.

Oil price Investment implications

The medium-term outlook points to continued caution among traders and portfolio managers.

Persistent oversupply and sluggish demand growth are likely to keep oil prices constrained, though periodic volatility should be expected as markets respond to policy and geopolitical events.

Producers with lower extraction costs and strong cash positions - particularly in the U.S. shale and Middle Eastern sectors - may remain relatively resilient, while higher-cost offshore projects could face profitability challenges. Refiners, on the other hand, could benefit from healthy processing margins if crude prices stay subdued.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why could oil prices fall to $55?

What could prevent a drop to $55?

How does refining activity fit into this?

Which countries are driving supply growth?