Trading calculator

Use Deriv’s trading calculators to calculate pip value, margin requirements, and swap charges on all your trades across Forex, Crypto, Commodities, Stocks, and more.

Deriv’s trading calculators

Quickly calculate the numbers behind your trade like required margin, pip value, and swap costs using tools that work across all Deriv platforms and markets.

Find the margin required to open a trade based on lot size and leverage.

Calculate pip differences for price movements.

Estimate overnight holding costs for long or short positions.

How do Deriv’s trading calculators work

1

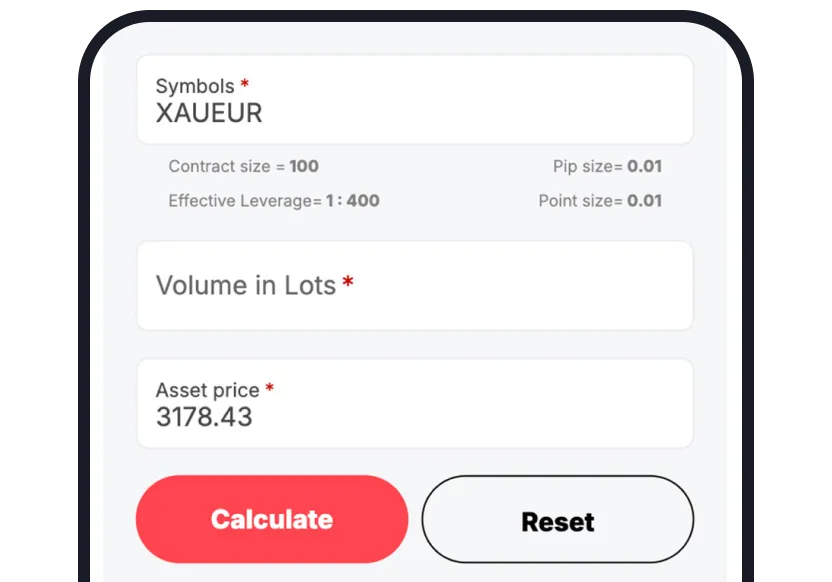

Enter your trade details

Select the instrument you want to trade, and input your trading volume in lots and asset price.

2

Confirm details

Once you are happy with your trading volume in lots and asset price, hit the calculate button.

3

View results

Get immediate results, including pip value, required margin, or overnight swap charges tailored to the asset you're trading.

Why use Deriv trading calculators

Deriv’s trading calculators simplify complex calculations so you can plan trades accurately and reduce risk.

Check trade costs in advance

Estimate margin, swap fees, and pip value before placing a trade to avoid unexpected charges.

Size your trades accurately

Use margin and pip calculators to adjust lot size based on your account balance and strategy.

Avoid margin calls and forced closures

Calculate required margin to ensure your account stays above the minimum margin level.

Your questions answered