Contents

Article

USD/JPY forecast: How long can Japan’s strong economy outlast ultra-loose policy?

October 22, 2025

Article

USD/JPY forecast: How long can Japan’s strong economy outlast ultra-loose policy?

October 22, 2025

Article

USD/JPY forecast: How long can Japan’s strong economy outlast ultra-loose policy?

October 22, 2025

Analysts suggest Japan’s economy can continue expanding under ultra-loose monetary policy - but only up to a point. Growth remains stable, inflation has exceeded the Bank of Japan’s 2% target for more than three years, and exports are regaining momentum.

Still, the BoJ’s cautious pace toward policy normalisation and a new government’s focus on fiscal spending are testing market patience. With USD/JPY hovering near 152, traders are asking whether Japan’s strong fundamentals can coexist with a soft currency, or if diverging Fed and BoJ policies will soon drive another push toward 160.

Key takeaways

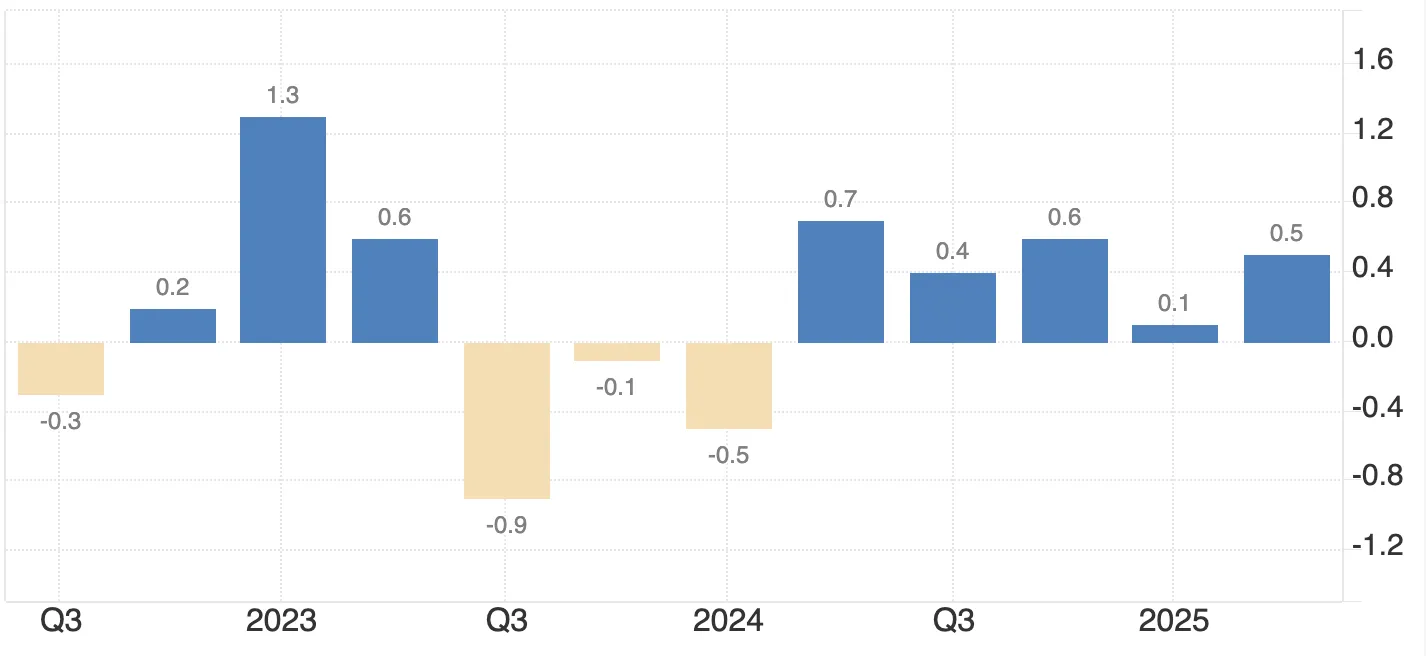

- Japan’s trade deficit narrowed slightly to ¥234.6 billion in September, from ¥242.8 billion in August, showing improvement but falling short of a projected surplus.

- Exports rose 4.2% year-on-year, the first increase since April, while imports climbed 3.3%, their first rise in three months.

- A Reuters poll shows 96% of economists expect BoJ rates to hit 0.75% by March 2026, with 60% forecasting a 25 bps hike this quarter.

- The election of Sanae Takaichi, Japan’s first female Prime Minister, boosted equities but weakened the Yen as traders priced in extended stimulus and delayed rate hikes.

- USD/JPY remains close to multi-decade highs, supported by Fed rate-cut expectations and uncertainty over Japan’s fiscal direction.

Japan fiscal stimulus optimism vs. fiscal constraints

The appointment of Sanae Takaichi marks a new chapter for Japan’s economic leadership - and a bold test of policy coordination. Her agenda centres on economic revitalisation, defence spending, and deeper U.S. ties, signalling readiness for fiscal expansion.

Her coalition with the Japan Innovation Party promised stronger stimulus to accelerate growth - reminiscent of earlier Abenomics-style policies. The Nikkei 225 surged nearly 13% since early October, briefly approaching the 50,000 mark before profit-taking pulled it back.

However, optimism about fiscal spending has added pressure on the Yen, as investors expect the BoJ to delay tightening. Yet, political limits remain - the ruling coalition holds 231 seats, just below the 233 needed for a majority, forcing Takaichi to rely on opposition support. That weak position could restrict her ability to push through large-scale reforms, leaving Japan’s economic outlook partly at the mercy of political negotiations.

Bank of Japan interest rates: Resilience defies policy inertia

Japan’s macro backdrop continues to surprise to the upside.

- The trade deficit narrowed for a second consecutive month, supported by improving export volumes.

- Exports rose 4.2% YoY, led by autos and electronics, while imports increased 3.3%, their largest jump in eight months.

- GDP has expanded for five straight quarters, confirming a durable recovery from 2023’s stagnation.

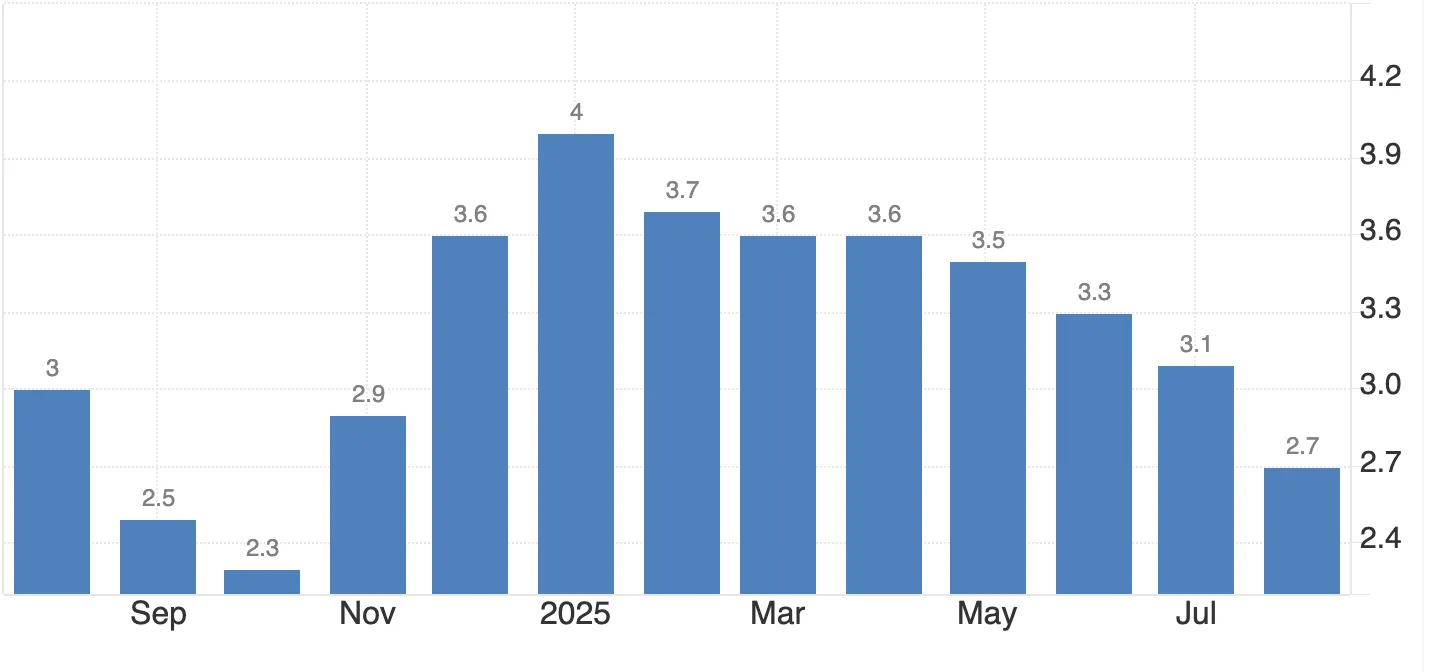

Inflation remains above 2%, driven by higher wages and resilient service demand.

Despite this, the BoJ remains the only major central bank with policy rates below 1%. Deputy Governor Shinichi Uchida has emphasised patience, saying rate hikes depend on “sustained inflation and wage growth,” while Board Member Hajime Takata noted that Japan has “largely met its price target.”

This cautious approach - against a backdrop of strong data - keeps the Yen under pressure as global investors chase higher yields elsewhere.

Japan’s policy rate: The slow road to 0.75%

Markets expect progress from the BoJ - but not speed. A Reuters survey of economists found 96% foresee Japan’s policy rate reaching 0.75% by March 2026, while 60% predict a 25 bps hike this quarter.

This gradual path highlights how the BoJ prioritises sustainability over reaction. Policymakers remain focused on ensuring wage gains are permanent rather than one-off responses to inflation. Still, this deliberate pace risks turning patience into inertia, leaving the Yen exposed if other central banks ease faster.

Across the Pacific: Fed cuts, fiscal chaos, and Dollar fatigue

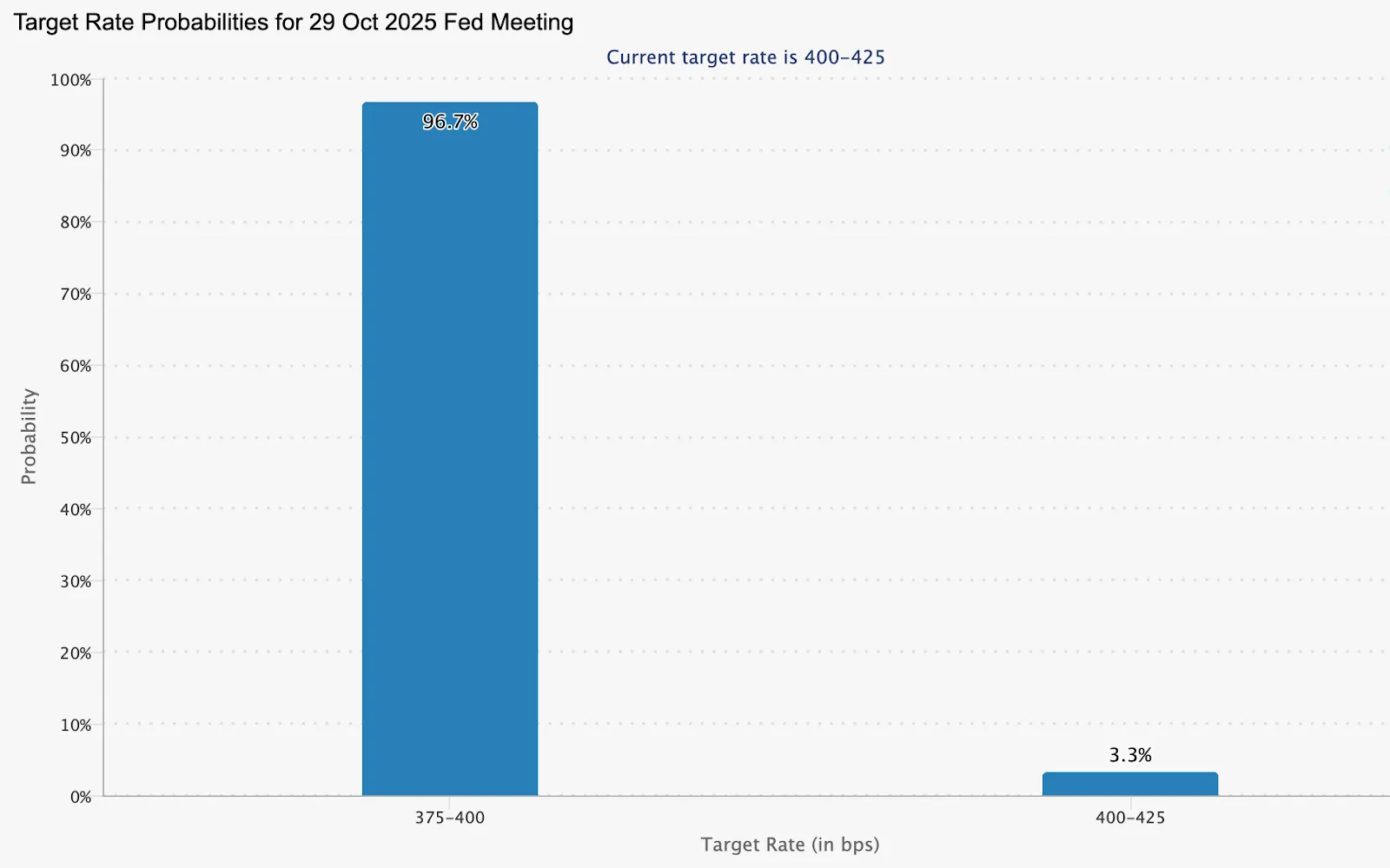

The U.S. Dollar Index (DXY) has slipped near 98.96, weighed down by growing expectations of two rate cuts and political gridlock. The U.S. government shutdown, now in its fourth week, has frozen data flow and clouded visibility on economic conditions.

The Senate’s 11th failure to pass a funding bill makes it the third-longest shutdown in modern U.S. history. The CME FedWatch Tool now prices in a 96.7% chance of a rate cut in October and a 96.5% chance of another in December.

Fed officials remain dovish:

- Christopher Waller backs another near-term cut.

- Stephen Miran calls for faster 2025 easing.

- Jerome Powell says the Fed is “on track” for a further quarter-point reduction.

With the U.S. slowing and the BoJ holding steady, the interest rate differential between the two economies is narrowing - limiting further Dollar upside even without BoJ intervention.

USD/JPY technical analysis: Between fiscal hope and policy drag

The appointment of Finance Minister Satsuki Katayama, who favours a stronger Yen and views 120–130 per USD as fair value, has balanced expectations for Japan’s currency. However, overall sentiment still leans toward weakness.

Analysts at Commerzbank say Japan’s new government is unlikely to deliberately weaken the Yen further, projecting sideways trading as BoJ caution offsets fiscal expansion.

After modest gains midweek, the USD/JPY pair trades near 151.84. A bullish breakout faces resistance at 153.05, while downside support sits at 150.25 and 146.70. The RSI (Relative Strength Index) shows improving buy momentum, suggesting short-term support for the pair.

Traders can analyse these levels using Deriv MT5 or Deriv’s Advanced Chart tool, which allows overlays of BoJ rate expectations and USD/JPY price action.

They may also use stop-loss orders to manage exposure near key support zones. Checking Deriv’s economic calendar can help anticipate major BoJ or Fed events that could drive short-term volatility.

Market impact and trading implications

For traders, USD/JPY continues to balance opportunity and risk.

- Upside scenario: If the BoJ remains on hold while the Fed delays cuts, USD/JPY could retest 158–160, testing policy tolerance for Yen weakness.

- Downside scenario: If the BoJ tightens ahead of expectations and the Fed cuts twice by year-end, the pair could fall back to 145–147, retracing part of its 2024 gains.

The carry trade remains a key force. With Japan’s rates still low, global investors borrow in Yen to invest in higher-yielding currencies. Any BoJ surprise or rise in volatility could trigger carry trade unwinding, driving sharp Yen appreciation.

Traders can monitor these dynamics with Deriv MT5. Ultimately, Japan’s economy looks strong - but its currency’s patience may be wearing thin. As 2025 unfolds, the key question isn’t whether Japan can grow, but how long its monetary stance can defy market gravity.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why hasn’t the Yen strengthened despite strong economic data?

Could USD/JPY really test 160 again?

What would it take for the Yen to recover meaningfully?

How does Japan’s new leadership shape monetary expectations?

How do U.S. policies influence Japan’s currency outlook?