Contents

Article

Gold price outlook: Central banks are holding the line

November 21, 2025

Article

Gold price outlook: Central banks are holding the line

November 21, 2025

Article

Gold price outlook: Central banks are holding the line

November 21, 2025

Gold’s resilience near $4,050 per ounce is proving difficult to shake, according to reports. Beneath the surface noise of shifting rate-cut bets and dollar strength lies a deeper structural trend: relentless central-bank demand. From Beijing to Warsaw, policymakers are steadily building their gold holdings, using the metal as a shield against political risk, currency volatility, and declining confidence in the U.S.-led financial order.

This official-sector buying has become the quiet stabiliser in bullion markets. Even as speculative flows taper and ETF demand plateaus, sovereign buyers are anchoring prices. With the People’s Bank of China logging its 12th straight month of accumulation - and other central banks joining in - gold’s price floor looks increasingly supported by nations rather than funds, according to analysts.

What’s driving gold right now?

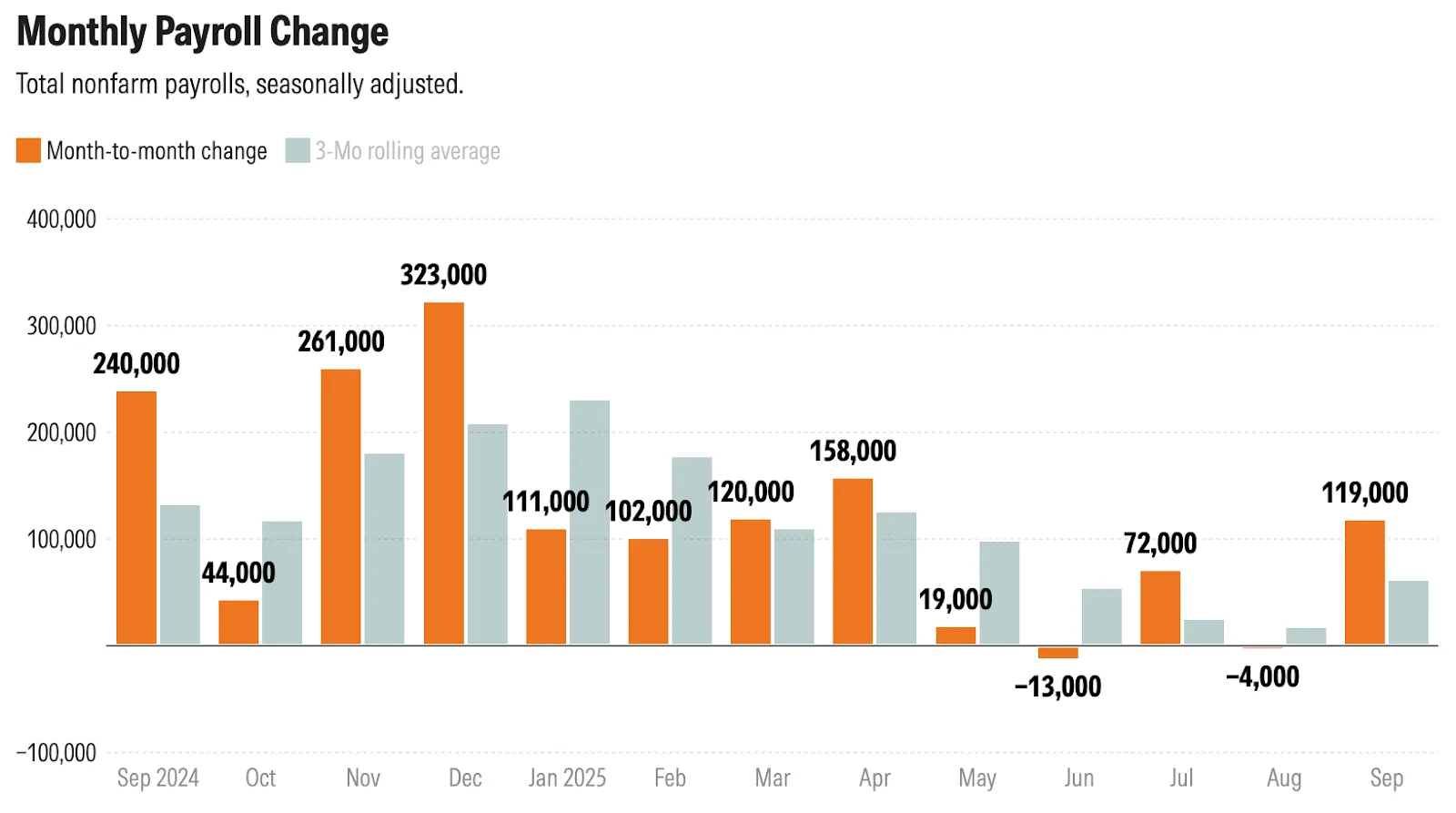

Recent U.S. labour data has shaken up expectations for monetary policy. The September Nonfarm Payrolls report revealed a 119,000-job gain, more than double forecasts, while unemployment ticked up slightly to 4.4%.

The mixed report was strong enough to temper hopes of a December rate cut from the Federal Reserve, sending Treasury yields and the dollar higher - a typically bearish setup for gold.

Yet gold barely moved. That’s because central-bank demand is changing how the metal reacts to interest-rate cycles. According to the World Gold Council, official-sector purchases now make up nearly a quarter of total annual demand - a sharp structural shift from a decade ago. When investors hesitate, central banks continue to buy. The PBoC added another 0.9 tonnes in October, taking holdings to 2,304 tonnes, or around 8% of China’s FX reserves. Turkey, Poland, and India are following similar paths.

Why it matters

According to market watchers, this steady, state-led accumulation is quietly transforming the role of gold in the financial system. Once seen purely as a risk-off trade, gold has become a strategic reserve asset — a neutral store of value that sidesteps the geopolitical risks of the dollar. The 2022 freeze on Russian reserves marked a turning point, prompting many countries to diversify.

As Peter Grant of Zaner Metals notes, the latest U.S. employment data “confirms a slowing yet stable market - but that doesn’t reduce the appetite for safety.” For emerging markets, gold provides something paper assets cannot: protection from sanctions, inflation, and politics. For investors, this means gold’s price movements now reflect trust in global policy and currency credibility as much as they do yield expectations.

Impact on markets and investors

One of the most remarkable dynamics in this cycle is gold’s ability to stay near record highs even as the U.S. dollar index (DXY) trades at multi-month peaks. The classic inverse relationship has weakened - both assets are being bought as safe havens.

For short-term traders, this correlation breakdown complicates the strategy. With gold sitting about 7% below its October record of $4,380, momentum has cooled, but the long-term bid remains firm. ETF flows have softened slightly but show no major outflows, suggesting a steady hand among institutional investors.

Retail traders have lightened up, but official buyers have stepped in to fill the gap. For long-term investors, that shift implies that dips may now represent opportunities to build positions - particularly if policy uncertainty or global growth risks increase heading into 2026.

Expert outlook

Market strategists remain split on how far central-bank demand can carry the rally. Goldman Sachs still describes recent weakness as “a pause, not a reversal,” while UBS expects prices could rise toward $4,900 per ounce within two years if dedollarisation continues apace.

The main threat to that bullish view would be a strong and prolonged U.S. economy, prompting the Fed to stick with its “higher for longer” stance. That could dampen speculative demand. Still, gold’s performance speaks volumes - it’s adapting to a world where monetary credibility and sovereign diversification matter more than rate expectations.

Gold technical analysis

At the time of writing, XAU/USD is trading close to $4,030, just above key support at $4,020. The RSI sits near the midpoint, reflecting market indecision and a lack of clear momentum.

Meanwhile, Bollinger bands are narrowing, signalling reduced volatility after recent swings. Prices remain near the mid-band, hinting at a consolidation phase before the next directional move.

On the upside, resistance sits around $4,200 and $4,365, levels where profit-taking or renewed buying could emerge if sentiment strengthens. A break below $4,020, however, could expose the next support area near $3,940, where stronger selling pressure may surface.

Key takeaways

Gold’s stability through late 2025 isn’t luck - it’s design. The same institutions that once parked reserves in Treasuries are now stacking bullion as insurance against political and economic shocks. Traders may take profits, but central banks are quietly defining the price floor. As the Fed faces conflicting signals and reserve patterns shift east, the foundation under gold looks increasingly state-built - and surprisingly steady.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why is gold holding steady even as rate-cut expectations fade?

Which central banks are leading the buying?

Does a stronger dollar still hurt gold prices?

Will gold reach $4,000?

Is gold still a safe haven for private investors?