Contents

Article

Why gold prices are signalling recession risks in 2025

September 22, 2025

Article

Why gold prices are signalling recession risks in 2025

September 22, 2025

Article

Why gold prices are signalling recession risks in 2025

September 22, 2025

Gold at $3,700 per ounce is more than just a record-setting figure - it’s a signal of mounting recession risks in the United States. According to Moody’s Analytics, the probability of a U.S. recession now stands at 48%, the highest since the 2020 pandemic. That warning comes alongside a weakening labour market, the Federal Reserve’s first rate cut of 2025, and persistent inflationary pressures. Analysts suggest that should a downturn materialise, gold could climb another 10–25%, testing the $4,000–$4,500 range by mid-2026.

Key takeaways

- Recession probability at 48% as payroll data revisions show nearly 1 million fewer jobs created over the past year.

- Fed easing is lowering real yields, reinforcing gold’s role as a safe haven.

- Physical and central bank demand remain strong despite high prices.

- Treasury yields and a firmer dollar are short-term headwinds but unlikely to derail the trend.

- Historical evidence shows gold typically advances - 25% in recession years.

Labour market stress points to a slowdown

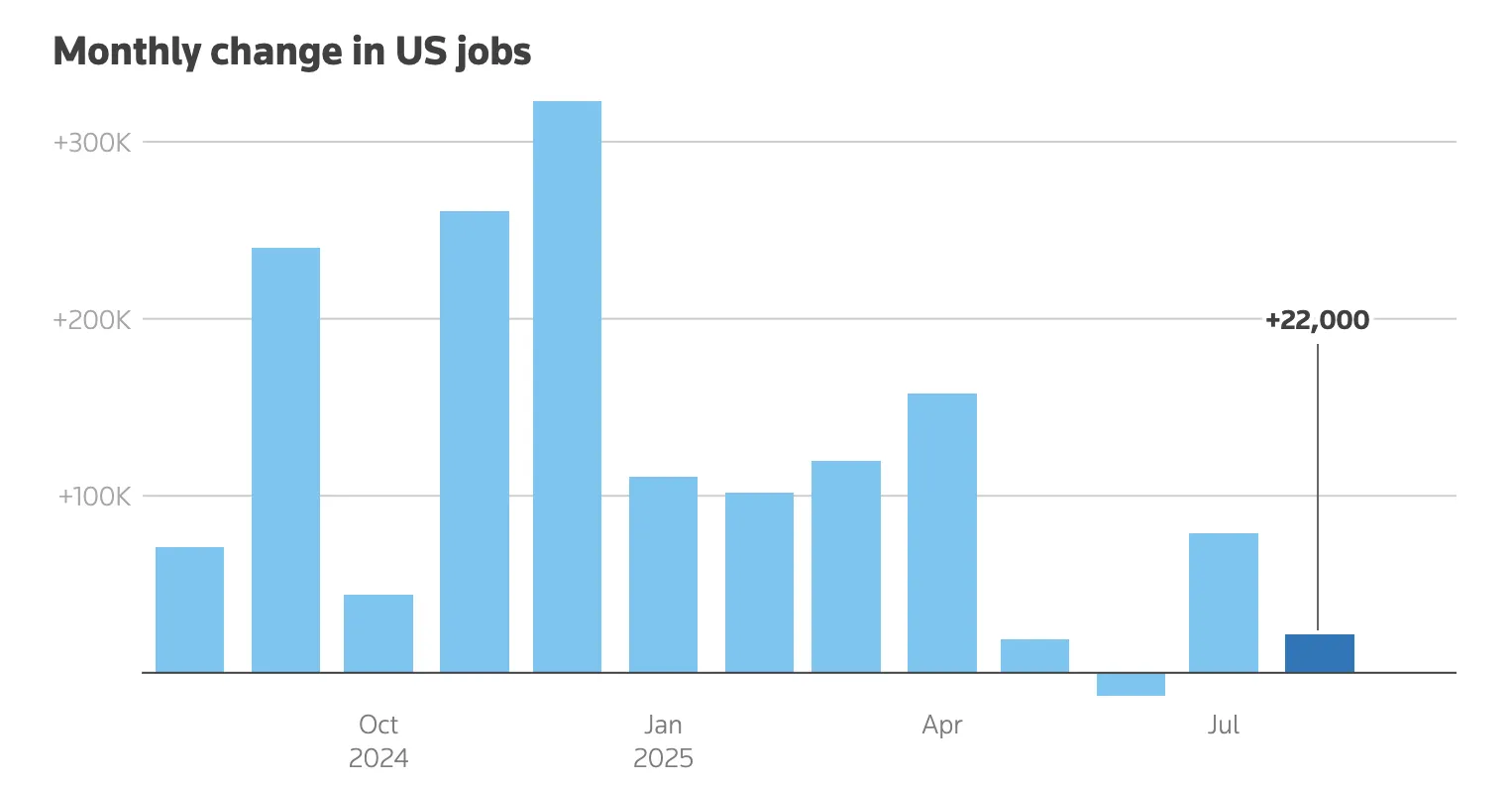

The labour market is central to recession concerns. Between April 2024 and March 2025, the Bureau of Labor Statistics revised down payroll figures by 911,000 jobs, with monthly job creation running below 100,000 for four straight months. Historically, such levels have coincided with the onset of recessions.

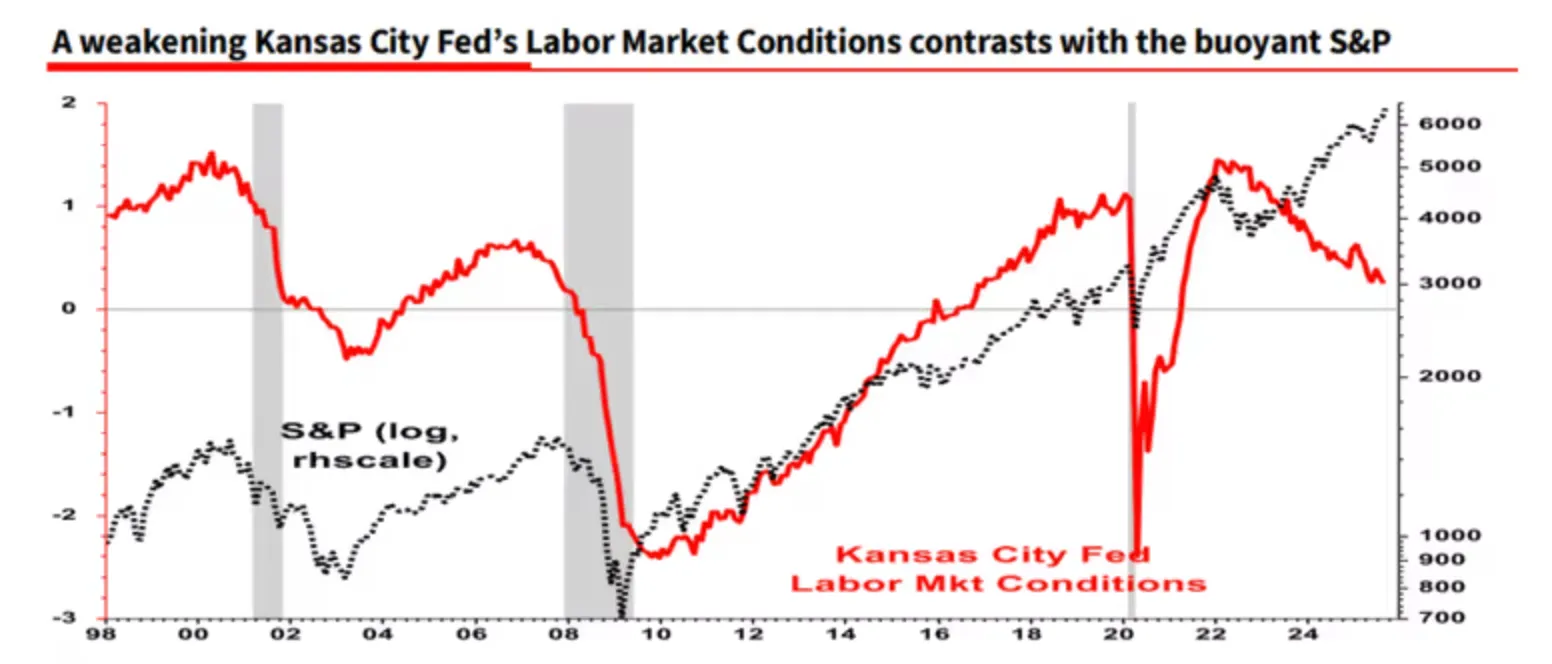

Moody’s chief economist Mark Zandi calls the probability of a downturn “uncomfortably high,” while Albert Edwards of Société Générale highlights broader red flags. The Kansas City Fed’s Labour Market Conditions Index - a composite of 24 employment metrics - has been in steady decline, a pattern consistent with past recessions, even as headline unemployment remains comparatively low.

Fed rate cut: a catalyst with caveats

The Fed’s decision to cut its policy rate by 25 basis points in September immediately drove gold to a record $3,707.40/oz. Chair Jerome Powell described the cut as a “risk-management” move, lowering the opportunity cost of holding gold. Minneapolis Fed President Neel Kashkari added that weak employment data justified the move and could warrant more easing in upcoming meetings.

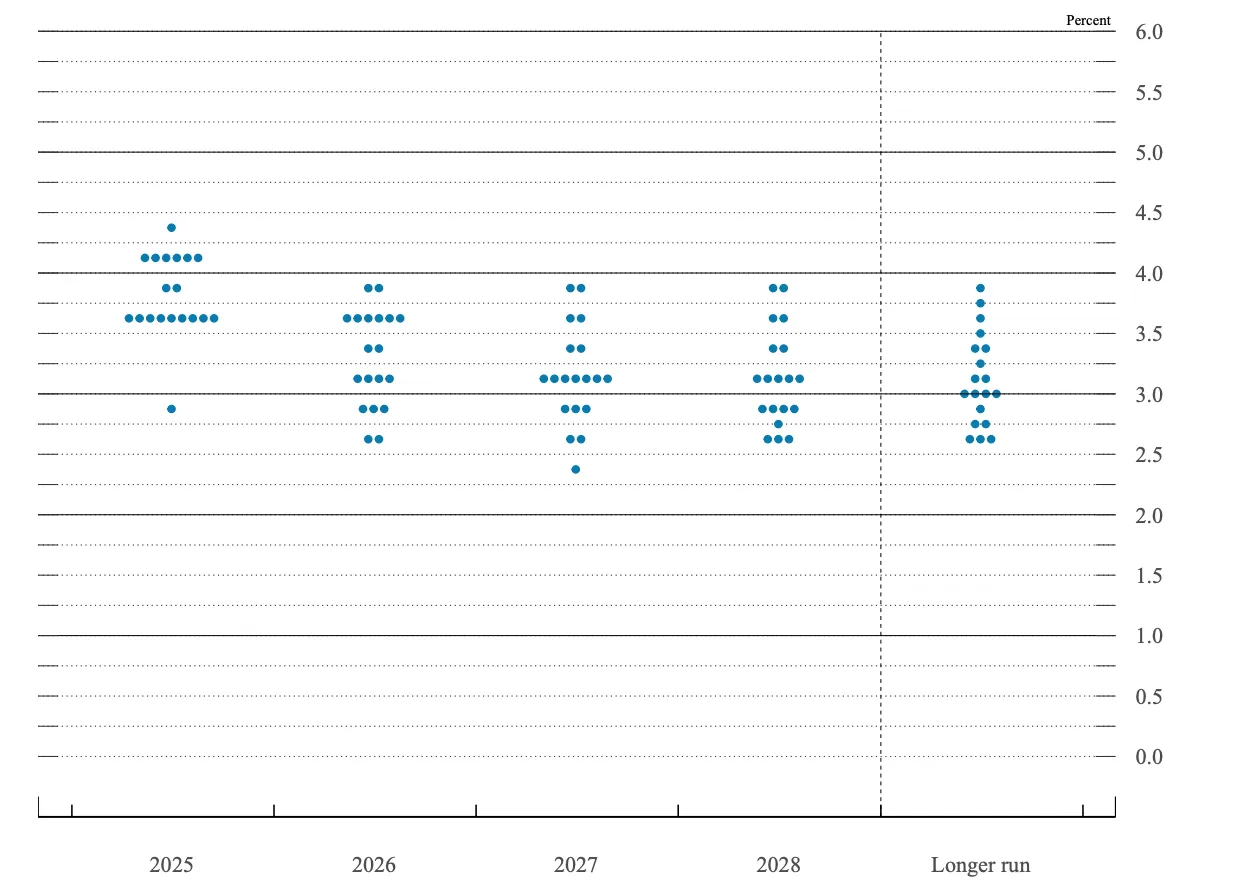

But the central bank has also been cautious. Inflation remains above 3%, aggravated by tariff-driven price pressures. The Fed’s latest dot plot suggests no more than two further cuts this year, a slower pace than markets anticipate.

Alt text: Federal Reserve dot plot showing policymakers’ projections for interest rates from 2025 through 2028 and the longer run.

Source: Federal Reserve

That mixed messaging has produced volatility: gold ended the week at $3,684.93/oz, still higher by 1.15% but well off its intraday highs.

RJO Futures strategist Bob Haberkorn argues the trend remains intact: “Gold is merely taking a breather after hitting new highs; the bull market trend remains intact, and reaching $4,000 by year-end is not out of the question.”

Yields and the dollar push back

The 10-year U.S. Treasury yield climbed to 4.12% last week, a rebound from earlier lows, after better-than-expected jobless claims and stronger regional manufacturing data. This drove a short-term correction in bonds and put upward pressure on the U.S. dollar.

The Dollar Index (DXY) rose 0.3% to 97.66 against the Yen, erasing earlier declines. According to strategist Marc Chandler, the Fed’s dovish tone contrasted with its hawkish rate path projections, creating a “bifurcated week” in FX markets.

For gold, higher yields and a stronger dollar raise near-term resistance. They increase the appeal of U.S. assets and make gold more expensive for international buyers. Still, analysts see these as temporary pressures: fiscal risks, divergent monetary policies abroad, and persistent inflation underpin demand for gold as a hedge.

Global demand and geopolitics: steady undercurrents

Gold’s strength is not just about U.S. policy. Physical demand and geopolitical risk are equally critical:

- India: Premiums surged to a 10-month high as festival season demand accelerated despite high prices.

- China: Discounts widened to a five-year high, underscoring weaker local appetite amid sluggish growth.

- Central banks: Net purchases remain strong, with a projected 900 tonnes to be added in 2025, reinforcing de-dollarisation trends.

- ETFs: Net inflows hit $38 billion in H1 2025, lifting holdings to record values, a 43% annual increase.

On geopolitics, conflicts in Ukraine, Gaza, and Poland, combined with U.S.–China trade tensions, continue to drive safe-haven flows. Analyst Rich Checkan describes these overlapping risks as a “perfect storm” for gold, particularly as U.S. debt climbs beyond $35 trillion, raising long-term concerns about dollar stability.

Historical precedent: Gold during economic downturn

Gold has a track record of strong performance in recessions:

- 2008–09: +25%, from $720 to $900, amid the financial crisis and near-zero rates.

- 2020: +25%, from $1,500 to $1,875, during the pandemic, and $6 trillion in stimulus.

- 2001: A mild slowdown brought only a modest +5% gain.

The 2025 setup most closely resembles 2008, with debt sustainability concerns, policy easing, and heavy central bank buying forming the backdrop.

Gold price technical insights for UAE traders

At present, gold remains in price discovery territory after breaking new highs. Buyers are in control, but volume data indicates sellers are providing resistance. Should bearish momentum strengthen, consolidation could take prices back toward $3,630, with further support at $3,350 and $3,310 if a deeper correction develops.

Gold price investment implications

Gold’s resilience to economic and geopolitical uncertainty cements its role as a portfolio hedge. Traders and investors may consider allocations of 5–10% through ETFs, physical bullion, or mining equities. Analysts see a floor near $3,500, with upside potential toward $4,000–$4,500 if recession risks escalate. Key catalysts to watch include the Q3 GDP release on 30 October and the December FOMC meeting, which will shape expectations for 2026 policy.

Disclaimer:

Disclaimer: The performance figures quoted are not a guarantee of future performance.

FAQs

Could gold really reach $4,000 in 2025?

What risks could limit gold’s upside?

How do U.S. Treasury yields and the dollar affect gold?

What role do geopolitics play in gold’s outlook?