Contents

Article

Gold’s pullback deepens: Is the PCE set to spark the next rally?

December 4, 2025

Article

Gold’s pullback deepens: Is the PCE set to spark the next rally?

December 4, 2025

Article

Gold’s pullback deepens: Is the PCE set to spark the next rally?

December 4, 2025

Analysts note that gold’s retracement has intensified this week, interrupting a rally that has pushed the metal to repeated all-time highs in 2025. Spot prices drifted toward $4,190 per ounce during Thursday’s Asian hours as traders locked in gains and shifted into risk-averse mode ahead of Friday’s delayed PCE report - the inflation measure most closely watched by the Federal Reserve.

That anticipation has created a tense standstill. Markets are now pricing almost a 90% probability of a quarter-point cut next week, yet uncertainty around the inflation outlook continues to restrain new buying. With real yields softening, the dollar weakening, and central banks purchasing gold at their most aggressive pace so far this year, the key question is whether the PCE print will offer the catalyst needed for gold’s next major breakout.

What’s driving gold?

Gold’s latest decline reflects a cooling of momentum rather than any erosion in the broader bullish structure, according to analysts. After a blistering 60% year-to-date climb and a historic break above the $4,000 threshold, even a brief wave of profit-taking was enough to trigger sharper-than-usual price swings. Many traders prefer to wait on the sidelines until the Federal Open Market Committee confirms its policy direction, making the market more sensitive to macroeconomic noise.

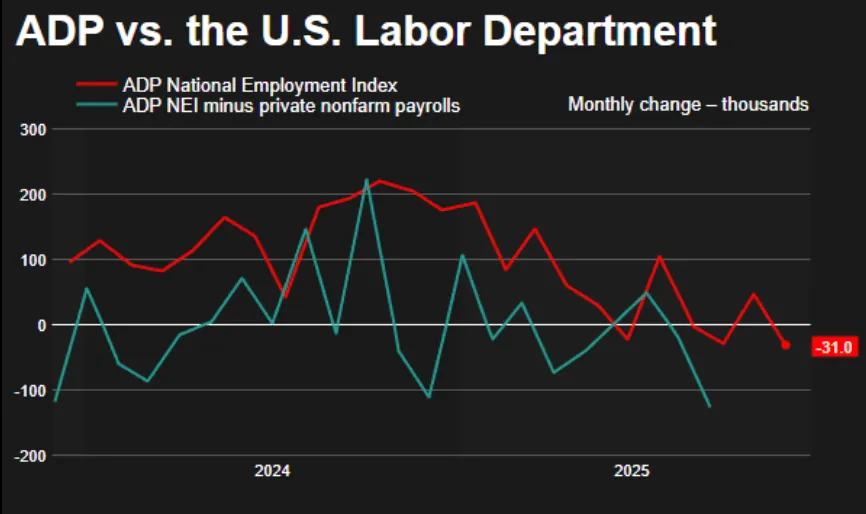

Soft labour data added to the caution. The ADP report showed a 32,000 fall in private payrolls - the largest drop in more than two and a half years - fuelling speculation that the labour market may be losing momentum more rapidly than expected. That weakness reinforces expectations of additional policy support from the Fed.

Currency dynamics have layered further complexity onto the gold narrative. Reports suggesting White House adviser Kevin Hassett could succeed Jerome Powell sent the US dollar to its lowest level since October, with the Dollar Index dipping to 98.86.

While a weaker dollar often amplifies gold’s upside, data suggests that traders appear reluctant to respond forcefully without clear confirmation from inflation data. Until the PCE report indicates a sustained easing in price pressures, the market seems unwilling to chase new highs.

Why it matters

The current pullback highlights how firmly gold is now tethered to expectations around US monetary policy. Real yields eased to roughly 1.83%, typically a supportive factor for precious metals, yet the hesitation among traders shows how sensitive the market has become to the smallest shift in inflation sentiment.

ANZ strategist Soni Kumari observed that the market “needs a fresh trigger” to extend the rally, noting that any retreat toward $4,000 is likely to draw strategic buyers back in.

Gold’s recent behaviour also reflects a broader reassessment of US economic resilience. The ISM Services PMI held at 52.6, hinting at ongoing expansion, but slowing orders and weak employment metrics point to uneven conditions beneath the surface. With fiscal concerns mounting and the dollar losing momentum, institutional investors are increasingly viewing gold as a hedge against policy uncertainty and potential currency volatility.

Impact on markets and investors

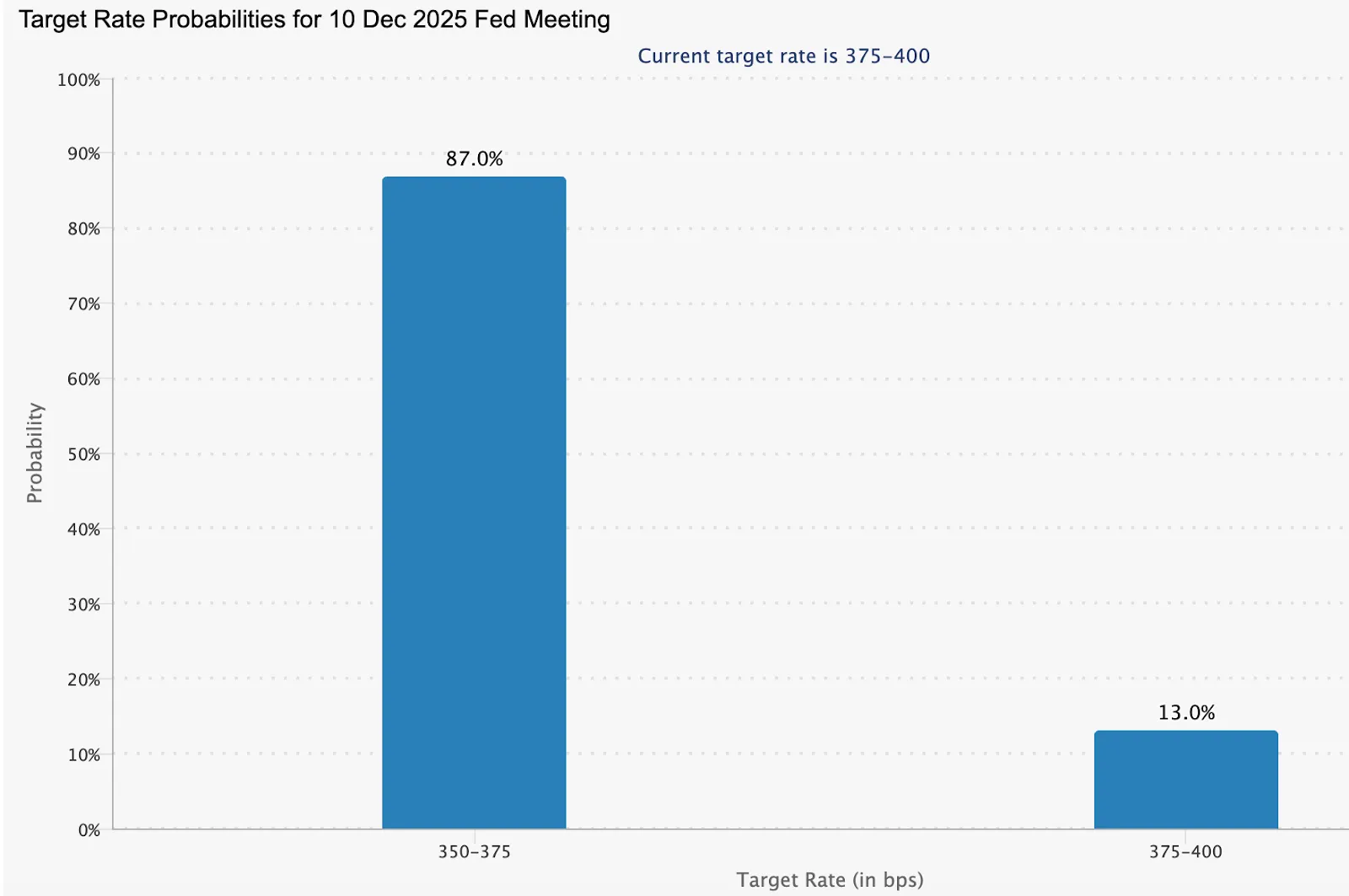

Financial markets are already adjusting ahead of a likely shift in Fed policy. Futures markets price roughly an 87% probability of a December cut, with nearly 89 basis points of easing expected by the end of 2026 - a trajectory that places the projected Fed Funds Rate near 2.99%.

This reset has pushed the 10-year Treasury yield down to around 4.06%, reinforcing the appeal of assets that do not rely on yield to attract capital. Lower real rates reduce the opportunity cost of holding gold, strengthening its appeal as a long-term diversifier.

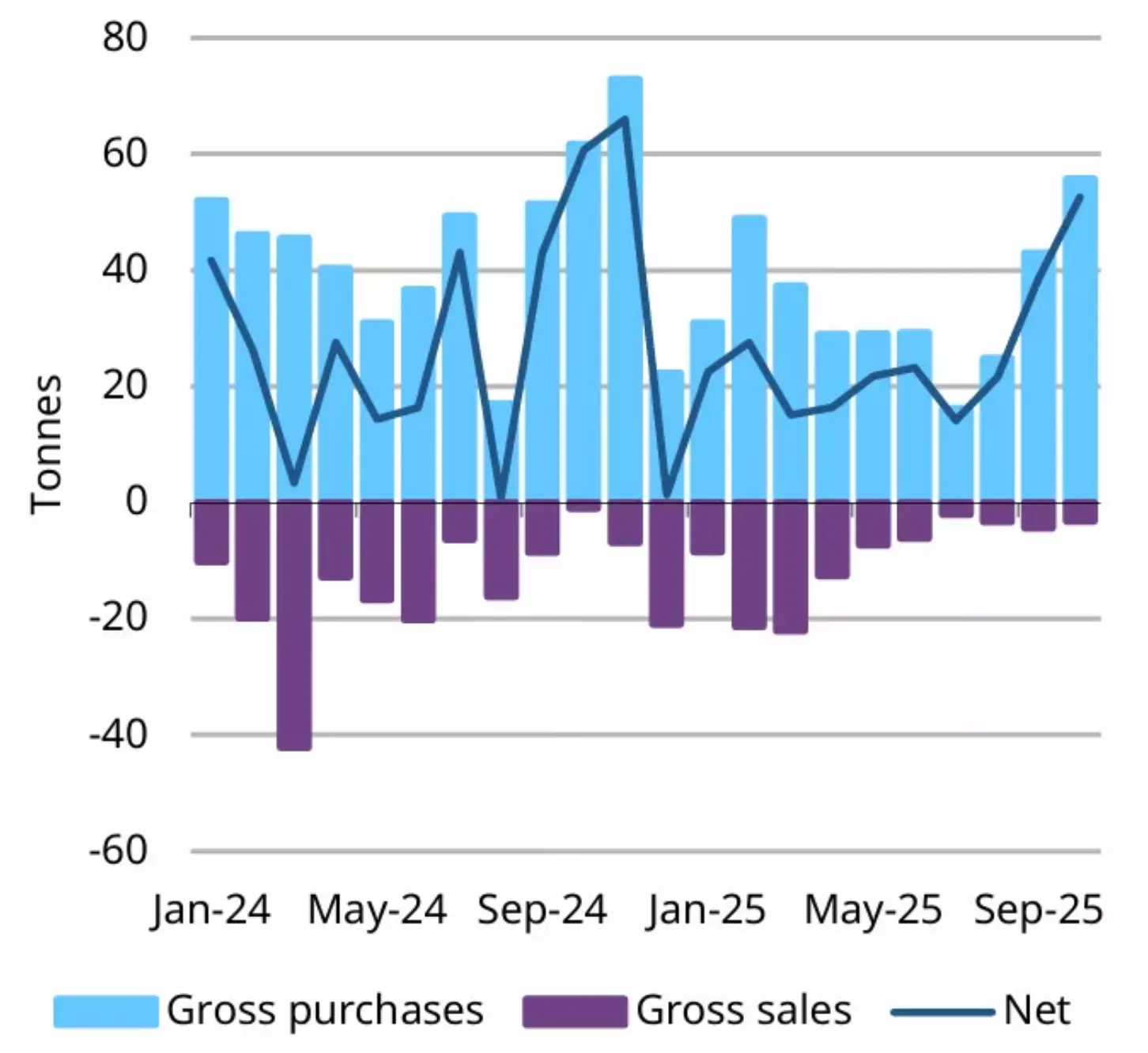

Structural demand is playing an equally important role. Central banks added 53 tonnes of gold in October - the strongest monthly figure of 2025 - led by renewed purchases from Poland. The broader trend shows reserve managers steadily shifting away from US-dollar-denominated assets, creating a cushion beneath gold during periods of market uncertainty.

This period is particularly pivotal because of the contrast between near-term restraint and long-term conviction. Institutional surveys indicate that nearly 70% of global investors anticipate gold prices to rise in 2026. That mix of caution and confidence suggests that a meaningful data catalyst - such as the PCE - could quickly reignite bullish momentum.

Expert outlook

Most analysts remain firmly optimistic about gold’s medium-term prospects. Goldman Sachs forecasts prices approaching $4,900 by the end of 2026, driven by what it calls “sticky purchases” from central banks seeking to insulate themselves from fiscal and currency risks. In a poll of more than 900 clients, 36% expected gold to exceed $5,000 by 2026, while only a small fraction anticipated a drop below $4,000.

JPMorgan sees gold climbing to roughly $5,055 by late 2026, while Morgan Stanley projects the metal at around $4,400 by the end of next year. Despite the bullish tone, analysts warn that progress will not be linear. The PCE data, next week’s Fed decision, and jobless claims figures will play a defining role in shaping the short-term path. If the data confirm easing inflation, gold’s next leg higher may begin sooner than expected.

Key takeaway

Gold’s pullback reflects a pause rather than a reversal. Real yields continue to soften, the dollar remains under pressure, and central banks are expanding their reserves at a historic pace - all conditions that typically support higher gold prices. The PCE report now stands at the centre of the narrative, with the potential to set expectations for next week’s Fed meeting and determine whether gold’s next surge takes shape. Traders will be watching closely for evidence that inflation is cooling and that the rate-cut cycle is firmly on course.

Gold technical insights

At the time of writing, Gold (XAU/USD) trades near $4,190, easing slightly after failing to break the $4,240 resistance zone. This level, along with the higher $4,365 region, has acted as a magnet for both profit-taking and burst-style buying when momentum accelerates. On the downside, support levels sit at $4,035 and $3,935 - a break beneath either could trigger broader liquidations and deepen the correction.

The broader structure remains constructive. Gold continues to hold above key support areas despite earlier overbought conditions, suggesting the market is entering a short consolidation phase while awaiting stronger macro catalysts. The RSI has slipped from overheated levels and is now drifting toward the mid-range near 70, signalling cooling bullish momentum rather than outright reversal. The MACD remains positive but is flattening gradually, reinforcing the idea that momentum is slowing but not breaking. A decisive close above $4,240 would be needed to revive the strong upward impulse.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why is gold pulling back now?

Does the PCE Index really move gold?

How do rate cuts affect gold prices?

What is the role of central banks in this rally?

Could gold really break above $5,000?

Is the US dollar still influencing gold prices?