Contents

Article

Is Intel’s historic rally the beginning of a turnaround or just market noise?

September 19, 2025

Article

Is Intel’s historic rally the beginning of a turnaround or just market noise?

September 19, 2025

Article

Is Intel’s historic rally the beginning of a turnaround or just market noise?

September 19, 2025

.webp)

Intel’s 23% surge - its biggest one-day gain since 1987 - has reignited debate about whether the chipmaker is on the cusp of a genuine turnaround or if the move is merely market noise driven by political and corporate headlines. The rally, powered by Nvidia’s $5 billion investment and the U.S. government’s earlier $8.9 billion stake, added $23.7 billion to Intel’s market capitalisation in a single day. While these endorsements have reshaped sentiment, Intel’s unprofitable foundry business and continued reliance on TSMC highlight that sustainable recovery will depend on execution, not headlines.

Key takeaways

- Intel shares jumped 22.77% to $30.57, the largest one-day rally in nearly four decades, boosting its market value by $23.7 billion.

- Nvidia invested $5 billion at $23.28 per share, securing an ownership stake of about 4%.

- The U.S. government bought a 10% stake for $8.9 billion in August at $20.47 per share, already showing a 54% paper profit.

- Intel and Nvidia will co-develop CPUs for AI data centres and PC chips integrated with Nvidia GPUs.

- Intel’s foundry remains unprofitable, with no major external customers, leaving the U.S. dependent on TSMC.

- Analysts are split: some see a “game-changer,” while others warn it is a rally without fundamentals.

Intel’s stock rally explained

The immediate catalyst was Nvidia’s $5 billion stake in Intel, bought at $23.28 per share. This followed the U.S. government’s purchase of 433.3 million shares in August for $8.9 billion at $20.47, giving Washington a 10% stake. Together, these moves injected nearly $14 billion of new capital and provided Intel with backing from both the U.S. government and the world’s most valuable chipmaker.

The announcement was coupled with a product partnership. Intel will design custom CPUs for Nvidia’s AI data centres and develop PC processors that integrate Nvidia’s RTX GPUs. For a company that has spent years lagging behind rivals in critical markets, this collaboration was enough to reframe Intel’s role in the AI landscape.

Political support added further weight. President Trump has pledged 100% tariffs on imported semiconductors, excluding firms that build products in the U.S. By investing directly in Intel and tying its fortunes to America’s chip sovereignty strategy, Washington has made clear that the company will not be left to collapse, despite losses of $19 billion in 2024 and ongoing restructuring.

Can Intel sustain the momentum?

The bullish case argues that Intel has been given a second life. With both Washington and Nvidia invested, the company now has political protection and commercial validation.

Analysts at Wedbush called the deal a “game-changer,” while CCS Insight described it as a “strategic alignment” that sets Intel on a clearer path. The government’s stake has already delivered paper profits of more than $4.4 billion, while Nvidia’s investment has gained $700 million.

For Nvidia, the deal provides strategic insurance at a time when China is banning its latest AI chips. By collaborating with Intel, Nvidia diversifies away from sole reliance on Arm for CPUs and ensures a U.S. ally has the capital to remain in the AI race. If these joint projects deliver, investors see scope for Intel’s stock to push toward $40–$45 in the coming quarters.

The unresolved risks: Intel’s foundry business

Despite the optimism, Intel’s structural weaknesses remain. Its foundry business, regarded as critical to U.S. supply chain sovereignty, continues to lose billions. Intel has yet to secure the “significant external customer” it says is necessary to keep investing in leading-edge manufacturing. Without this, it may retreat from the foundry race, leaving the U.S. dependent on Taiwan’s TSMC.

Even Nvidia’s chief executive, Jensen Huang, downplayed speculation that his firm would become an Intel foundry customer. He praised TSMC as a “world-class foundry” and confirmed both companies would continue to rely on it. That admission highlights the gulf between Intel’s geopolitical role and its commercial reality.

Geopolitics adds further volatility. Just a day before Nvidia’s announcement, China ordered its largest tech firms to halt testing and cancel orders for Nvidia’s RTX Pro 6000D chips. This underscored how sensitive chip valuations are to political manoeuvres. For Intel, the danger is that its stock remains driven more by global power struggles than by its own fundamentals.

Intel stock surge and market scenarios

The Nvidia deal reshaped the market in one session. Intel’s stock soared by 22.77% to $30.57, Nvidia rose 3.5%, and Arm fell 4.5% as investors recalibrated partnerships. The U.S. government’s stake is now worth around $13.3 billion, up from $8.9 billion, while Nvidia’s holding is valued at about $5.7 billion.

In the bullish scenario, Intel capitalises on its new alliances, develops competitive AI and PC chips, and secures foundry customers, sustaining higher valuations into 2025.

In the bearish case, execution falters, foundry losses persist, and the rally fades, sending the stock back into the mid-$20s and leaving September’s surge as a historical outlier.

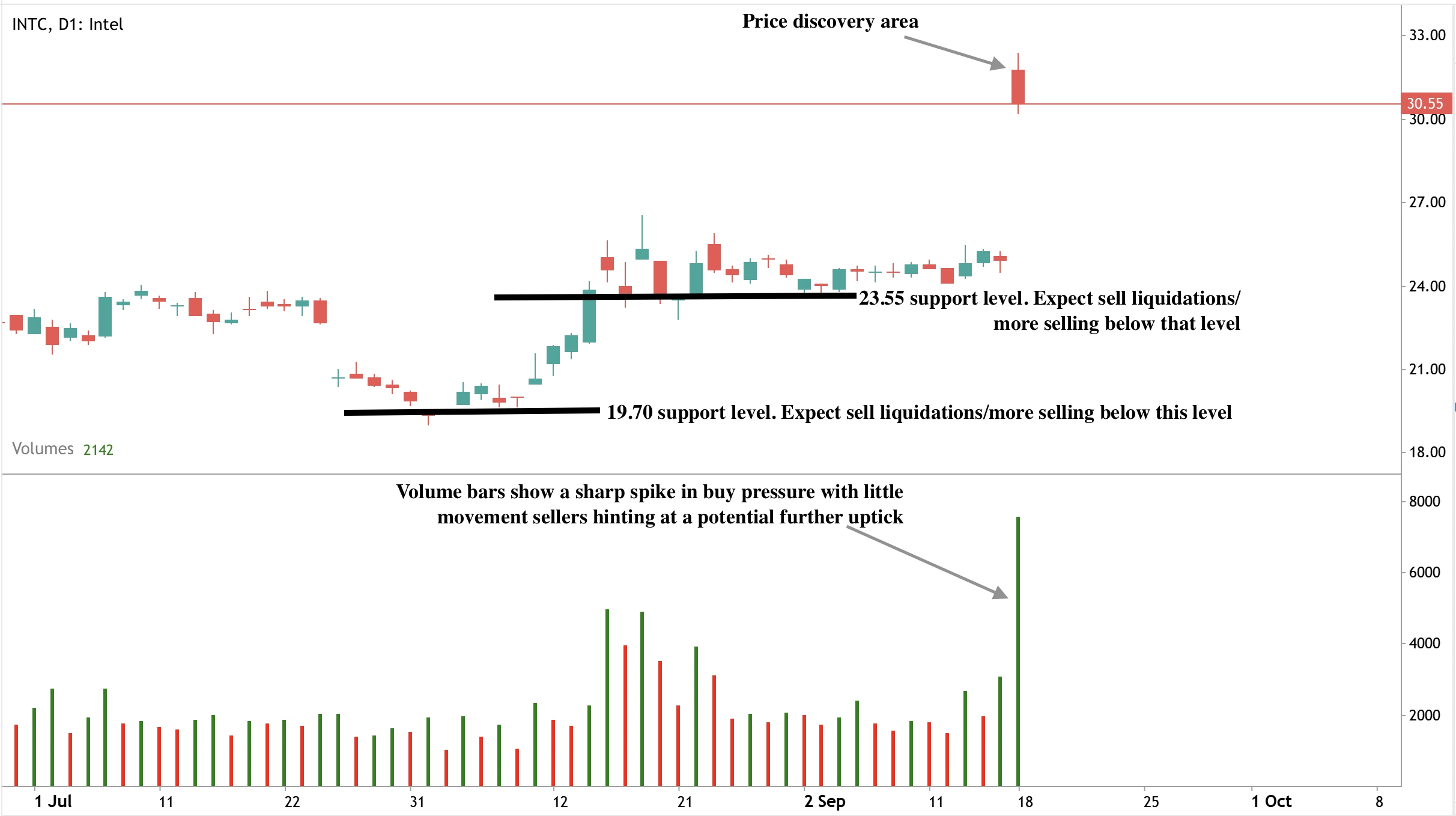

Intel stock technical analysis

At present, Intel shares are consolidating just above $30 after their sharp move. The $29.50–$30.00 level is acting as near-term support, but recent red candles suggest profit-taking is underway. If the stock can hold this range, resistance at $34.50 and $40.00 would be the next levels to watch. A breakdown below $29.50 could send shares toward $27.00, and deeper retracements might test $23.50 or even $19.70, unwinding much of the gap-up. The technical picture is consistent with the fundamentals: strong short-term momentum but fragile sustainability.

Investment implications for Intel stock traders

For traders, the $30 level is a key pivot point. Holding above it could provide short-term upside to $34.50 and $40, while a break lower could trigger a return toward $27. For medium-term investors, caution remains warranted. Intel’s rally rests on political capital and Nvidia’s endorsement, but its structural weaknesses - particularly in the foundry - remain unresolved. For portfolio managers, Intel may be attractive as a U.S.-backed strategic asset in the semiconductor arms race, but until operational results improve, it is better viewed as a speculative turnaround play rather than a proven AI leader.

Trade the next movements of Intel with a Deriv MT5 account today.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why did Intel’s stock rally so sharply?

Does this mean Intel is back as a technology leader?

What role does geopolitics play in Intel’s surge?

What are the main risks to Intel sustaining its rally?

Is this a sustainable rally or just market noise?