Contents

Article

Nvidia beats expectations: Is the AI boom back on track?

November 20, 2025

Article

Nvidia beats expectations: Is the AI boom back on track?

November 20, 2025

Article

Nvidia beats expectations: Is the AI boom back on track?

November 20, 2025

Yes - analysts say the AI boom isn’t over; it’s maturing. Nvidia’s latest earnings didn’t just calm nerves; they proved that artificial intelligence is moving from hype to hard numbers.

The chipmaker’s stronger-than-expected results marked its first sales acceleration in seven quarters, sparking renewed optimism across tech markets and restoring faith in AI’s staying power.

For months, investors fretted about “peak AI.” But Nvidia’s results - record-breaking data centre revenue, strengthened partnerships, and a 5% jump in after-hours trading - tell a different story. The AI economy isn’t collapsing; it’s settling into a new phase of measured, sustainable growth.

What’s driving Nvidia’s momentum

Nvidia’s resurgence stems from the same engine that built its empire - data centres. The division’s revenue exceeded $50 billion this quarter, beating expectations and underscoring the global demand for AI infrastructure. This surge represents industrial buildout, not speculative excitement.

From powering ChatGPT to handling enterprise-scale cloud workloads, Nvidia’s GPUs have become the indispensable hardware of the AI era. As CEO Jensen Huang remarked, “We’re in every cloud.” That ubiquity gives Nvidia its moat. With Blackwell GPUs delivering up to 40 times faster inference speeds than their predecessors, the company continues to set the benchmark for computational efficiency rather than chasing market fads.

Why it matters

Nvidia’s report now serves as the pulse of the broader AI economy. Its earnings beat wasn’t simply about profit margins - it was about perspective. The market had priced in fear after weeks of tech volatility, but Nvidia’s results brought back realism.

Julian Emanuel of Evercore ISI summed it up neatly: “The angst around ‘peak AI’ has been palpable.” Those doubts evaporated once Nvidia demonstrated that AI demand is still expanding. With artificial intelligence now a structural growth driver across industries, the company’s consistency signals endurance, not exuberance. Its $5 trillion valuation last month wasn’t excess - it was foresight.

Impact on global markets

The ripple effects were immediate. Global tech indices that had sagged on AI fatigue turned higher as Nvidia reignited investor confidence. Asian markets opened stronger, and S&P 500 futures flipped positive overnight. Even after heavy corrections - with Meta and Oracle each losing nearly 20% - Nvidia’s performance reminded traders that the long-term AI growth story remains intact.

Beyond equities, Nvidia’s success underscores a shift in capital priorities. Its multibillion-dollar partnerships with Microsoft, OpenAI, and Anthropic are more than strategic alliances - they represent long-term bets on AI infrastructure. Each investment deepens a self-reinforcing cycle of innovation, data capacity, and model development that drives both revenue and relevance.

Expert outlook

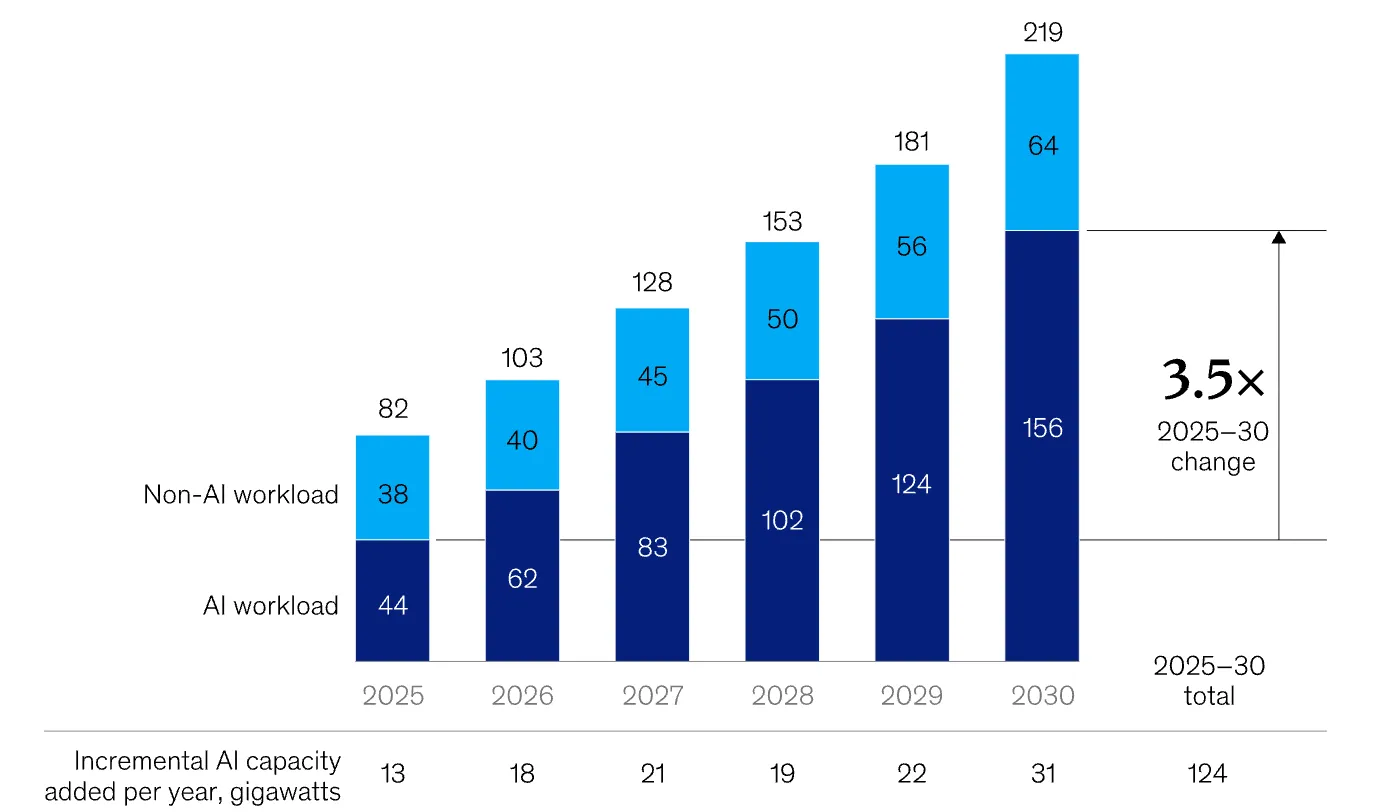

Forecasts for AI investment are being rewritten. McKinsey projects $7 trillion in AI infrastructure spending by 2030, with $5.2 trillion dedicated to data centres alone. Each year, new capacity is expected to multiply, fuelling the next wave of machine learning breakthroughs.

Nvidia is well-positioned to capture a significant share of that spending - analysts estimate up to 50%, thanks to its early lead in design and manufacturing. Some even see a potential $20 trillion valuation by 2030 if innovation continues at the current pace. However, challenges remain. Export restrictions to China, increased competition from AMD and Google, and global chip supply tensions could test Nvidia’s dominance. Yet its CUDA software ecosystem, which binds developers to its hardware, remains its greatest defence.

Nvidia technical analysis

At the time of writing, Nvidia’s stock (NVDA) trades near $186, showing renewed strength after a brief consolidation. The RSI is climbing above 50, signalling rising bullish momentum as investors re-enter the market.

Meanwhile, the Bollinger Bands are narrowing - a typical prelude to a breakout. The stock is hovering near its mid-band, suggesting equilibrium before a potential move. Support zones lie at $180 and $168, while resistance around $208 marks the level to watch for confirmation of a sustained uptrend.

Key takeaway

Nvidia’s potential earnings beat isn’t another euphoric moment - it’s a validation of AI’s real-world demand. The company’s results reinforce that the industry has outgrown its speculative phase and is now building long-term infrastructure. The conversation is shifting from “is AI real?” to “how fast can it scale?”

For traders navigating this evolving landscape, Deriv MT5 offers a professional platform to engage with tech markets. Tools like the Deriv trading calculator help manage exposure and fine-tune strategies in this fast-changing environment.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Can we be certain that we’re in a bubble?

What caused Nvidia’s share price to spike after earnings?

Why is Nvidia so critical to the AI industry?

What are the key risks for Western AI chipmakers?

How sustainable is AI spending?