Contents

Article

Sanctions vs oversupply: Oil’s battle between risk and reality

November 20, 2025

Article

Sanctions vs oversupply: Oil’s battle between risk and reality

November 20, 2025

Article

Sanctions vs oversupply: Oil’s battle between risk and reality

November 20, 2025

Oil prices are balancing on a knife-edge - pulled between geopolitical pressure and stubborn market fundamentals. With Washington’s latest sanctions on Russian oil giants like Rosneft and Lukoil now in play, the market is asking: will these restrictions finally curb supply enough to revive prices, or will record U.S. output and bloated inventories drag them back down?

WTI crude has been hovering around $60 a barrel, reflecting the prevailing mood of uncertainty. Each hint of tighter sanctions lifts optimism, but every inventory report brings traders back to earth. This standoff between politics and production will decide whether oil’s next move is a rally or another stalled recovery.

What’s driving the rebound

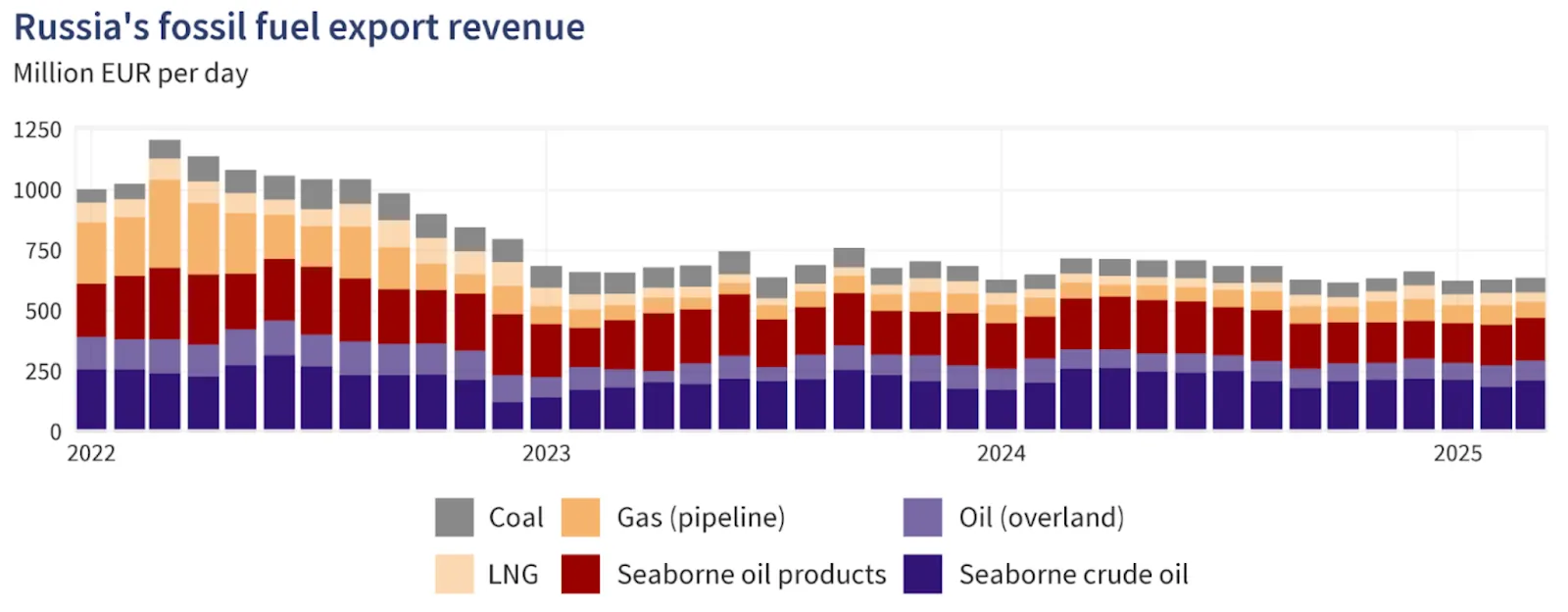

Oil’s modest rebound has been underpinned by renewed supply concerns, particularly over Russia’s ability to maintain its exports under fresh U.S. and European sanctions. The U.S. Treasury’s latest measures extend to hundreds of vessels in Moscow’s so-called “shadow fleet,” designed to choke off a key channel for Russian oil exports. The intended effect is clear: restrict Russia’s barrels, tighten global supply, and push prices higher.

But the market isn’t buying the full story. Despite these restrictions, Russia’s output has remained surprisingly stable, rising by about 100,000 barrels per day in recent months. Meanwhile, according to the International Energy Agency (IEA), non-OPEC+ producers are expected to add around 1.7 million barrels per day this year, outpacing demand growth of just 0.79 million bpd. The numbers paint a simple picture - the world still has plenty of oil. Until demand accelerates, every rally risks being fleeting.

Why it matters

This push-and-pull between sanctions and supply abundance carries consequences far beyond the trading floor. If sanctions truly bite, exporters could enjoy higher prices and stronger margins, while consumers face higher fuel bills and rising inflation.

However, if the oversupply narrative prevails, prices may remain capped, keeping inflation in check but hurting producers’ earnings. “The market doesn’t expect much lost supply until enforcement becomes indisputable,” one analyst noted, summing up the scepticism surrounding the sanctions’ bite.

For Russia, the economic stakes are high. Its oil and gas revenues plunged 27% in October 2025 compared with a year earlier, a sign of pressure even as volumes remained resilient through alternative trade routes. Meanwhile, India and China - Russia’s key buyers - ramped up imports earlier in the year, cushioning Moscow from sharper revenue declines.

As long as Asian importers continue to absorb discounted Russian crude, the global supply picture remains well-supplied. For consumers, that’s a double-edged sword - manageable pump prices now, but potential volatility if sanctions suddenly start to bite.

Impact on the market

Analysts see the oil market split between two dominant forces. If sanctions begin to meaningfully reduce Russian exports, a genuine supply squeeze could trigger a price rebound. Early signs suggest a shift: the discount on Russian Urals crude widened to around US$19 per barrel versus Brent in early November, hinting that sanctions are starting to sting.

Yet, satellite and shipping data show Russian oil still finding its way to buyers through rerouted cargoes. Meanwhile, the U.S. continues to pump record volumes, with inventories swelling across major hubs. In that context, oversupply remains the stronger gravitational pull. Unless industrial and transportation demand picks up, any rally driven by supply risk may quickly fade.

Refiners and traders are also adapting, opting for longer routes, higher insurance costs, and opportunistic purchases of discounted crude. However, until actual volumes decline, prices are likely to remain range-bound, with only brief bursts of volatility to disrupt the calm.

Expert outlook

For now, analysts expect oil to remain stuck in a sideways market - prone to short spikes on news of disruptions, followed by swift corrections as fundamentals reassert themselves. The IEA still forecasts global supply growth outpacing demand this year, underscoring the fragility of any bullish momentum.

That said, the outlook could shift fast if enforcement tightens - particularly if shadow-fleet tankers are barred or Asian importers scale back. On the demand side, stronger travel activity, industrial output, or a surprise uptick in China’s petrochemical consumption could add momentum. Until then, oil’s rally rests on thin ice.

Oil technical insights

At the time of writing, U.S. crude trades around $59.50 per barrel, consolidating within a narrow range as momentum stabilises. The RSI has climbed back above 50, signalling a slight uptick in bullish sentiment. Meanwhile, the Bollinger Bands (10, close) have tightened, suggesting reduced volatility and an approaching breakout.

Support is found near $58.26 and $56.85 - a break below these could trigger renewed selling. Resistance lies at $62.00 and $65.00, where buyers may test conviction if momentum builds. The setup points to a cautious market waiting for a catalyst - be it sanctions enforcement or a change in demand dynamics.

Key takeaways

Oil’s current equilibrium is fragile - caught between the political drama of sanctions and the economic reality of oversupply. While new restrictions on Russian exports inject risk into the market, resilient output, high inventories, and weak demand continue to weigh on prices.

Until Russian exports show a sustained decline and consumption recovers, oil’s rally will remain more talk than trend. The key signals to watch: Russia’s export data, global stockpile movements, and any rebound in Asian demand. This tug-of-war isn’t over - but for now, oversupply still holds the stronger grip.

For traders navigating the oil market, Deriv MT5 offers exposure to both WTI and Brent. Meanwhile, tools such as the Deriv trading calculator provide the precision needed to manage risk as the AI-driven market matures.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Will the Russian sanctions immediately reduce global oil supply?

Why aren’t oil prices already surging if supply is under threat?

How are buyers in Asia affecting the sanctions story?

What would trigger a sustained oil rally?