Contents

Article

US Indices outlook improves as Greenland risks cool

January 22, 2026

Article

US Indices outlook improves as Greenland risks cool

January 22, 2026

Article

US Indices outlook improves as Greenland risks cool

January 22, 2026

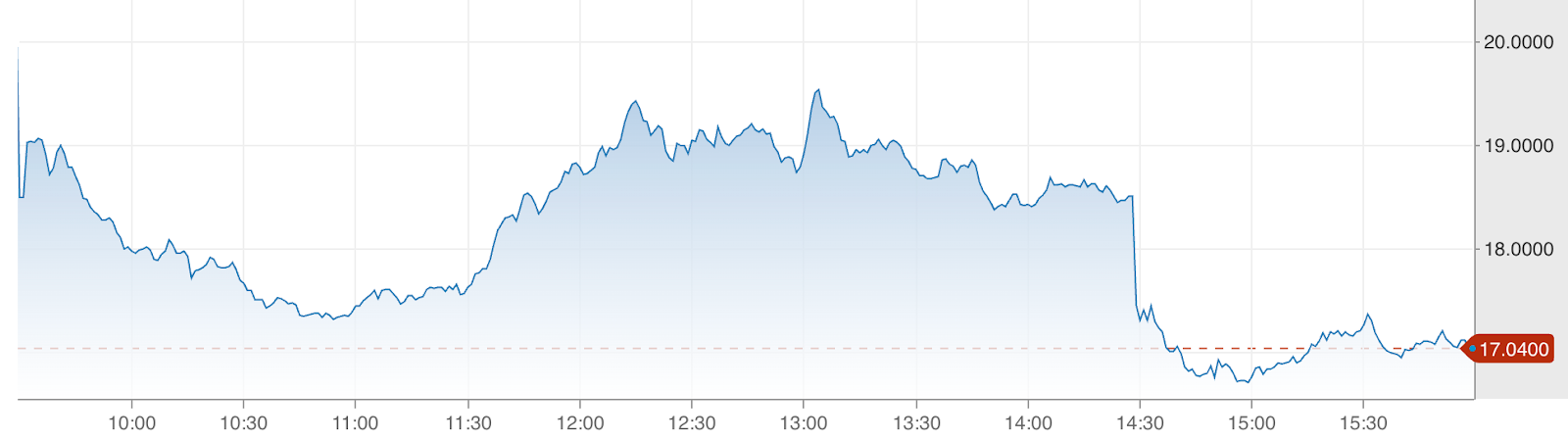

US stock indices steadied this week as Wall Street rebounded from a sharp pullback, helped by a cooling of geopolitical tensions linked to Greenland. A rapid easing of tariff-related fears encouraged investors back into risk assets, reversing part of the recent sell-off.

The S&P 500 advanced roughly 1.2% to around 6,875, while both the Dow Jones Industrial Average and the Nasdaq Composite posted similar gains during Wednesday’s session. The rebound followed President Trump’s decision to step back from previously signalled tariff measures, which had unsettled markets earlier in the week.

The recovery extended into futures trading, hinting at a more constructive near-term tone as investors refocus on upcoming inflation data and a busy earnings calendar. While geopolitical risk has faded for now, market participants are increasingly focusing on economic indicators that will determine whether the rebound has staying power.

What’s driving the market outlook?

The change in tone stems from a swift reversal in risk sentiment after President Trump clarified that tariffs tied to his Greenland ambitions would not be imposed on European trading partners. That clarification helped unwind a sharp risk-off move that had taken hold at the start of the week.

Speaking at the World Economic Forum in Davos, Trump referenced a potential “framework” for future NATO cooperation, signalling a more diplomatic approach. Although details remain sparse, the comments reassured investors that a broader trade confrontation could be avoided, at least in the near term.

Earlier tariff threats had weighed heavily on index futures, boosting demand for safe havens such as gold. The pivot away from escalation reduced immediate downside risks and opened the door to bargain hunting, allowing the S&P 500 and Nasdaq to claw back lost ground. Still, markets are navigating a crowded macro landscape, with a key personal consumption expenditures (PCE) inflation reading and major earnings reports looming large.

Why this matters to investors

The rapid swing in sentiment highlights just how reactive equity markets have become to policy signals. When tariff rhetoric intensified, equities faltered, and volatility spiked, reflecting widespread risk aversion. The subsequent rebound illustrates how quickly those positions can reverse once uncertainty eases.

Analysts note that relief rallies can reveal deeper shifts in investor psychology. Broad participation across major indices, including small caps and large-cap technology stocks, suggests that appetite for risk has not disappeared. Instead, it has become more selective, dependent on clearer macro guidance and fewer headline shocks.

Attention is now turning firmly to the economic backdrop. With inflation data and earnings from major corporates approaching, investors are weighing whether economic fundamentals justify current valuations. Supportive data could reinforce the rebound, while disappointment may quickly revive volatility.

Impact on markets and strategic positioning

The easing of tensions over Greenland has influenced how investors are positioning across sectors. Financials and energy stocks, which had been pressured during the risk-off phase, rebounded as bond markets stabilised and yields edged lower. Technology shares also advanced, though gains were more measured, suggesting renewed caution around growth valuations.

These sector moves offer insight into market confidence. Strength in more value-oriented segments points to ongoing belief in a soft-landing scenario for the US economy, even as inflation and policy uncertainty linger. If upcoming data confirms resilient demand and earnings strength, it could encourage more sustained flows into cyclical areas.

That said, fragility remains evident beneath the surface. Despite Wednesday’s rally, major indices are still mixed over the week. This contrast underscores that while geopolitical fears can fade quickly, structural challenges such as inflation pressures, interest-rate expectations, and corporate margins continue to shape investor behaviour.

Expert outlook

Looking ahead, the market’s focus is narrowing on several key catalysts. The upcoming PCE inflation report will be closely watched for clues about the Federal Reserve’s next steps. A softer reading could reinforce risk appetite, while upside surprises may revive concerns about tighter financial conditions.

Earnings season represents another crucial test. Results from major companies across technology, consumer, and industrial sectors will be scrutinised not only for headline beats but for forward guidance. In an environment where markets demand credible outlooks rather than short-term wins, guidance may matter more than past performance.

Strategists caution that volatility is unlikely to disappear. Geopolitical developments can resurface quickly, and macro data releases are set to carry outsized influence. For both traders and longer-term investors, flexibility and close attention to incoming signals will remain essential as the outlook evolves.

Key takeaway

US equity sentiment improved as Greenland-related tensions eased, fuelling a broad rebound across major indices. However, the market’s next direction will depend less on geopolitical relief and more on inflation data and corporate earnings. As attention shifts back to fundamentals, upcoming releases will play a decisive role in shaping volatility and leadership in the weeks ahead.

Disclaimer:

The information contained on the Deriv Market News is for educational purposes only and is not intended as financial or investment advice. The information may become outdated, and some products or platforms mentioned may no longer be offered. We recommend you do your own research before making any trading decisions. The performance figures quoted refer to the past, and past performance is not a guarantee of future performance or a reliable guide to future performance.

FAQs

Why did US stock indices rebound this week?

Are indices still down for the week?

What economic data could move markets next?

Does this rally signal a lasting turnaround?