Contents

Article

U.S. manufacturing decline impacts 2025 crude oil price trajectory

August 4, 2025

Article

U.S. manufacturing decline impacts 2025 crude oil price trajectory

August 4, 2025

Article

U.S. manufacturing decline impacts 2025 crude oil price trajectory

August 4, 2025

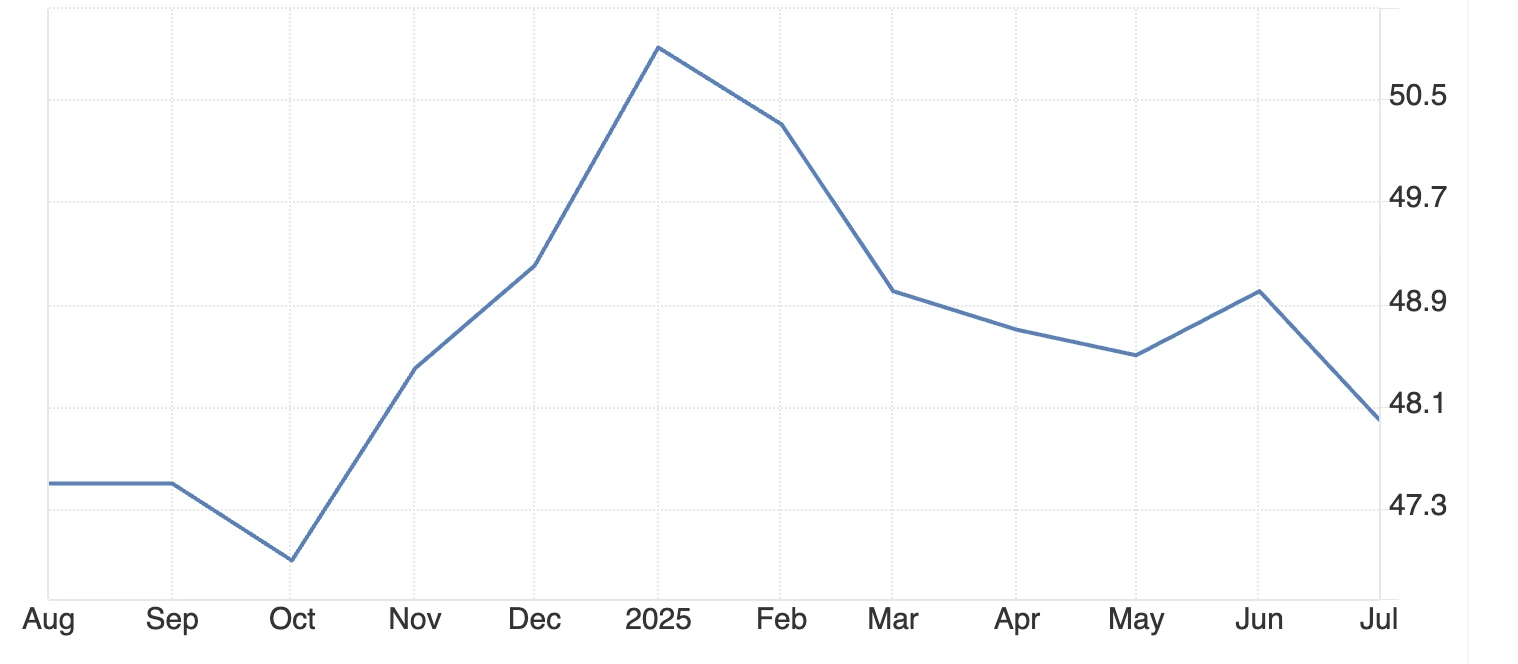

The protracted downturn in the U.S. manufacturing sector, now in its fifth month as of July 2025, has seen the Purchasing Managers' Index (PMI) dip to 48, triggering downward pressure on oil demand. Such trends, coupled with declining industrial activity, suggest crude prices might gravitate towards the $60-70 range, reminiscent of downturns in past economic cycles.

Key insights

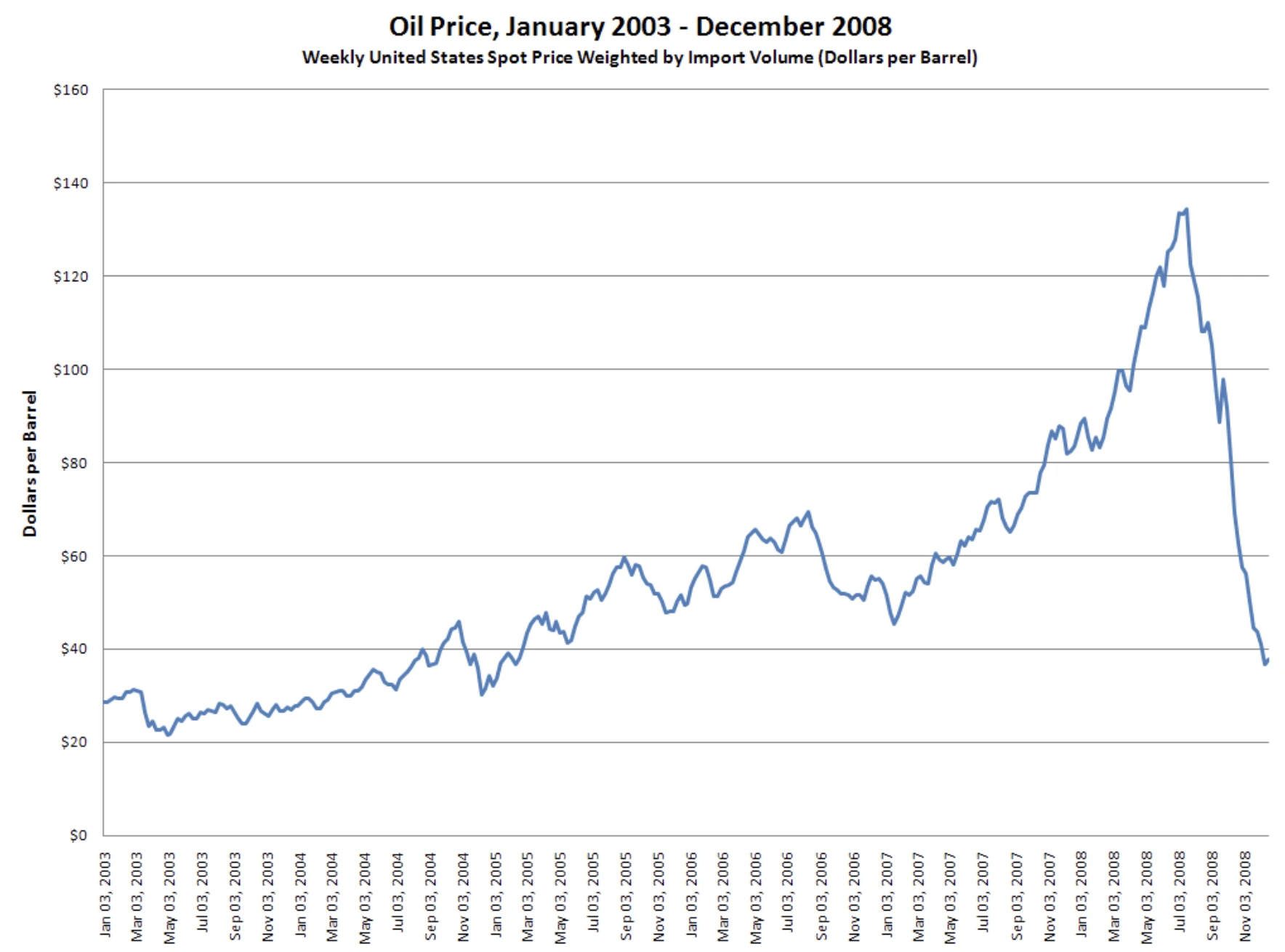

The sustained contraction of U.S. manufacturing, marked by a PMI of 48 in July 2025, poses a threat to global oil demand. Employment in this sector has plummeted by 25%, the steepest drop since the COVID-19 pandemic, alongside a six-month decline in new orders. The 2008 financial crisis offers historical context, as similar manufacturing weaknesses led to a collapse in oil prices from $147 to below $40 per barrel. Currently, crude oil is trading at approximately $66-67, with notable pressure pointing downwards, and key support and resistance levels identified at $64.58 and $69.80, respectively.

How U.S. manufacturing weakness is affecting industrial oil demand

Manufacturing significantly influences oil consumption through several channels. Heavy machinery operations rely on diesel, transportation networks utilise petroleum for goods movement, and supply chain logistics demand both gasoline and diesel when factories are fully operational. The July 2025 PMI reading of 48, below the neutral threshold of 50, directly correlates with diminished petroleum demand in industrial sectors. Data from the Institute for Supply Management reveal that manufacturing activity has declined in 31 of the last 33 months, maintaining sustained pressure on oil consumption.

A deeper look at employment data reveals structural issues. The manufacturing employment index fell to 43.4 in July 2025, the lowest since the pandemic. This reduction in workforce affects fuel demand for commuting, industrial production levels, and overall supply chain activity.

How past manufacturing crises shape oil price analysis

The 2008 financial crisis serves as a cautionary tale of how manufacturing contractions can impact oil markets, with crude prices plunging from $147 per barrel in July to under $40 by December that year as industrial demand withered. Present conditions echo this pattern, with experts observing sustained PMI readings below 50, rising input costs, and restricted business investments.

Typically, manufacturing downturns precede broader economic slowdowns, which significantly curtail oil demand. The ongoing five-month contraction mirrors early recession warning signs from past periods that led to notable crude price declines.

Oil market outlook: How U.S. tariffs and fed policy are weakening demand

Tariff policies are inflating input costs for manufacturing, while Federal Reserve interest rate policies limit business expansion. Higher production costs are curtailing industrial activity and logistics volumes, both key drivers of petroleum consumption. These policy factors exacerbate the underlying weakness in manufacturing.

Projections from the U.S. Energy Information Administration indicate a decline in crude oil production from 13.5 million barrels per day in April 2025 to 13.3 million barrels per day by the end of 2026. WTI crude prices are forecasted to drop to $53 per barrel by 2026, a 22% decrease from June 2025 levels.

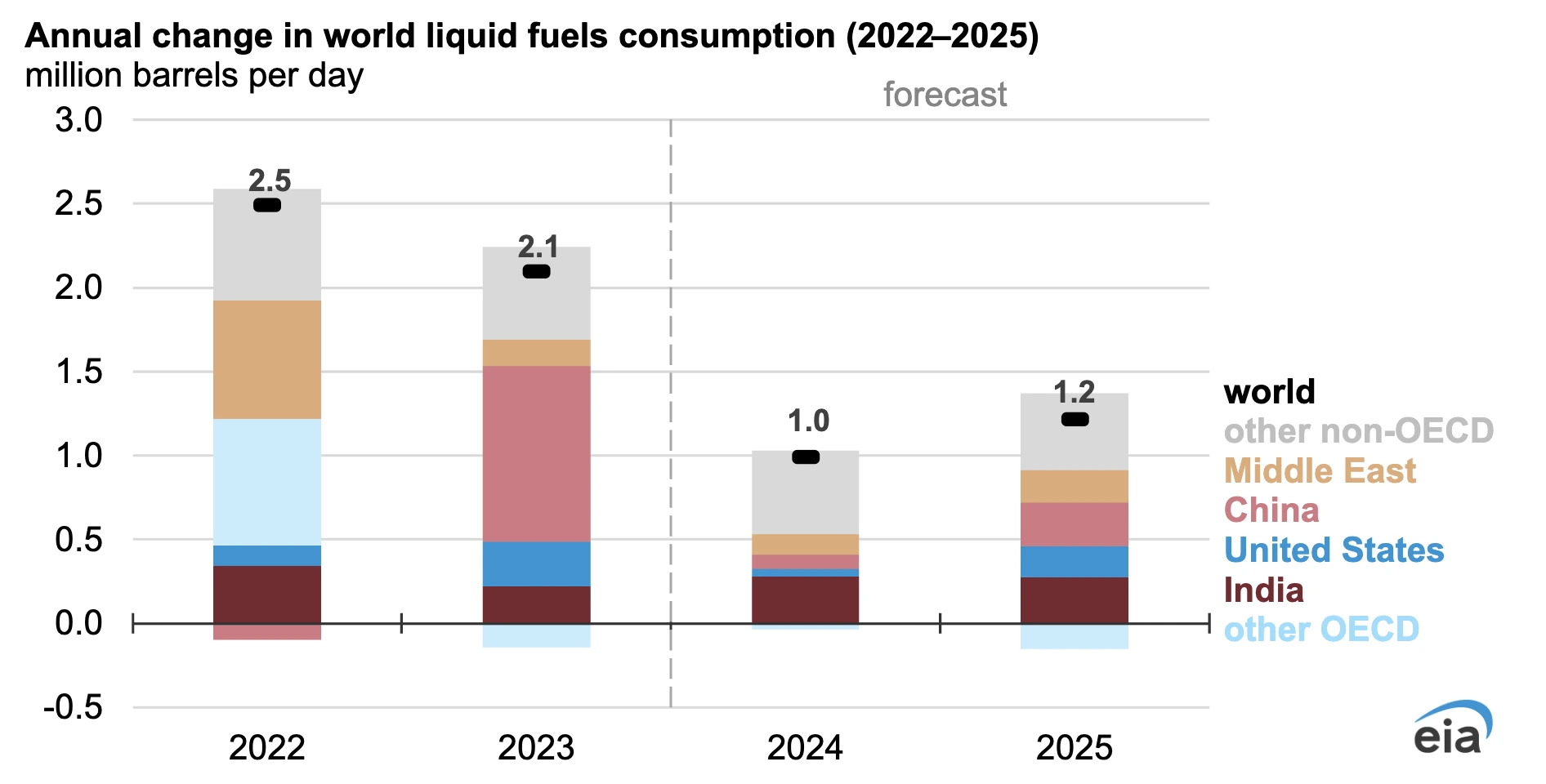

Can emerging market oil demand offset U.S. industrial slowdown?

In 2025, India's oil consumption reportedly rose by 3.1% to 5.6 million barrels per day, while China's decreased by 1.2% to 16.4 million barrels per day. However, emerging markets often rely on subsidised energy pricing, which offers limited support for global oil prices.

The shift of global manufacturing to lower-cost countries represents a reshuffling of demand rather than an actual increase. As the largest oil consumer, the U.S. industrial demand declines cannot be fully offset by emerging market consumption growth.

How OPEC+, Russia, and Middle East tensions could impact the oil price forecast

OPEC+ is slowly unwinding voluntary production cuts while global production remains stable at 101.8 million barrels per day. According to analysts, geopolitical tensions, such as the Israel-Iran conflict and potential secondary sanctions on Russian oil buyers, create upside price risks.

While supply disruptions could temporarily bolster prices, the ongoing manufacturing weakness suggests that demand-side factors will likely dominate market direction. Without significant geopolitical events, oversupply conditions may develop as industrial demand continues to decline.

Oil price outlook and trading levels

Current technical analysis indicates a recovery in oil prices from weekend lows, with emerging buying pressure. Resistance is identified at $69.80, while critical support is at $64.58. A breach below these support levels could hasten moves towards the $60-70 target range.

The EIA's forecast of $53 per barrel WTI by the end of 2026 aligns with the manufacturing-driven demand weakness. Declining U.S. production, paired with reduced industrial consumption, creates a bearish price environment in the absence of major supply shocks.

How will industrial decline influence oil prices in 2025?

PMI readings below 50 for five consecutive months indicate sustained industrial weakness. The six-month decline in new orders points to continued manufacturing contraction, while a 25% reduction in employment suggests decreased energy consumption across various sectors.

Without improvements in manufacturing conditions or significant supply disruptions, oil prices are likely to trend towards the $60-70 per barrel range. The quiet decline of U.S. industrial activity could have a more pronounced impact on crude price direction than dramatic geopolitical events.

Investment implications

Analysts suggest that manufacturing weakness could exert sustained downward pressure on oil prices through 2025. The $60-70 per barrel range is a realistic expectation in the absence of supply shocks. Geopolitical risks remain the primary catalyst for upward price movement, while manufacturing data points to continued demand headwinds.

Investors should monitor manufacturing PMI, employment data, and new orders as leading indicators of petroleum demand trends. Policy changes affecting trade or monetary conditions could alter the trajectory.

How do you think oil will fare? Trade oil movements today with a Deriv MT5 account.

Disclaimer:

The performance figures quoted are not a guarantee of future performance. This content is not intended for EU residents.

FAQs

How has the U.S. manufacturing sector been performing in 2025, according to the manufacturing PMI?

What is the EIA's oil price forecast through 2026?

How are global oil consumption patterns affecting the market outlook?

What factors that affect the price of oil could prevent it from falling to the projected $60-70 range?