Contents

Article

Why metals are rallying again amid deepening Fed uncertainty

December 18, 2025

Article

Why metals are rallying again amid deepening Fed uncertainty

December 18, 2025

Article

Why metals are rallying again amid deepening Fed uncertainty

December 18, 2025

%20(1).webp)

Metals are back in the spotlight as investors respond to a Federal Reserve that remains deliberately non-committal. Recent US labour data showed the unemployment rate edging up to 4.6%, the highest reading since 2021, while hiring momentum slowed noticeably. Inflation, however, is still running too hot for policymakers to declare victory. That uneasy balance between cooling growth and stubborn price pressures has prompted investors to return to precious metals.

Silver’s surge towards record territory around $66.50 per ounce, alongside platinum’s decisive break above multi-decade resistance, suggests this is more than a short-lived bounce. Markets are now increasingly pricing rate cuts in 2026, real yields are easing, and supply tightness is becoming harder to ignore. With investors awaiting further clarity from upcoming inflation data, metals have re-emerged as a key gauge of confidence in the global policy backdrop.

What’s driving the metals rally?

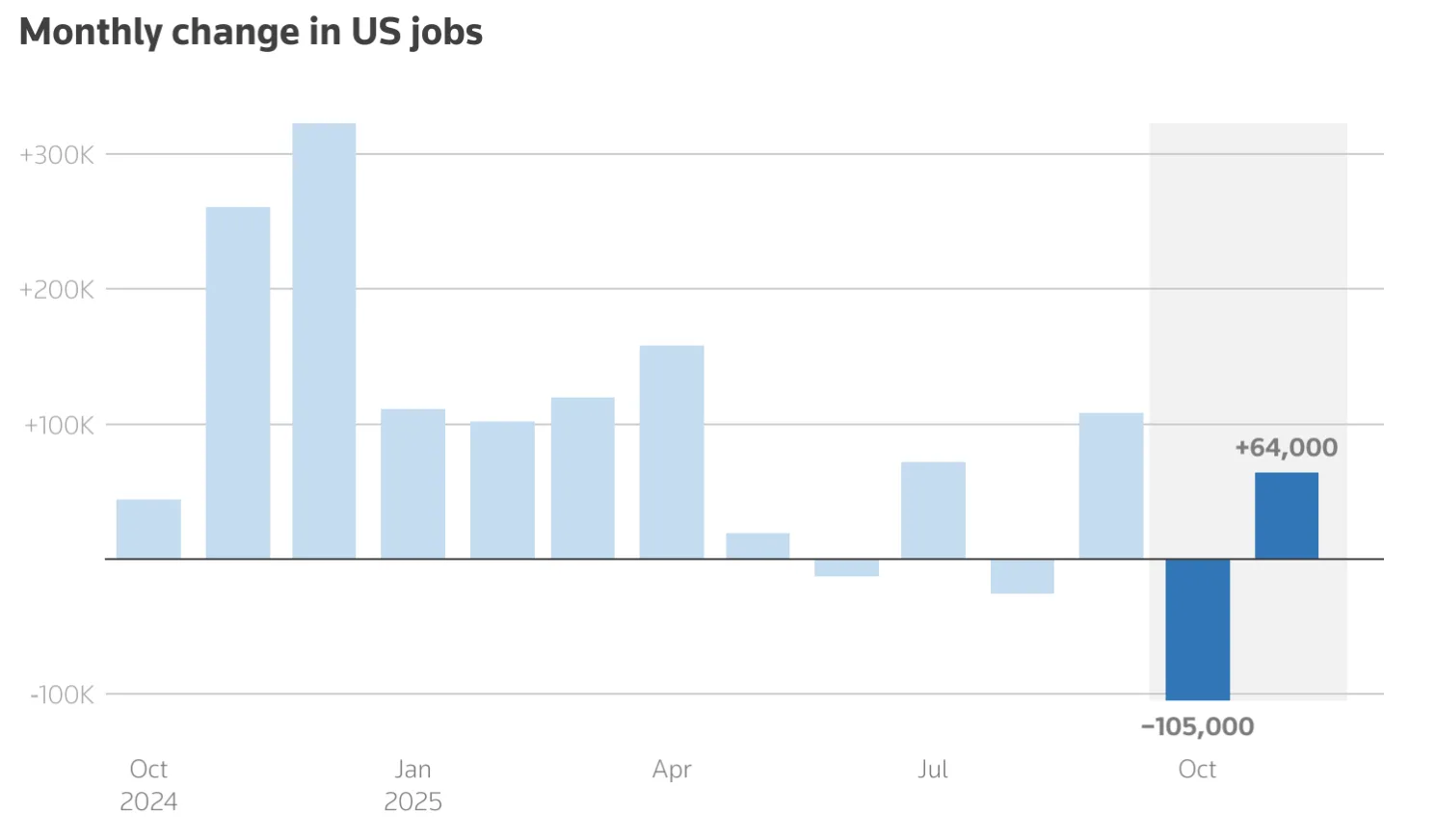

The renewed strength across metals stems largely from uncertainty surrounding the Fed’s next move. The latest Non-Farm Payrolls report indicated a labour market that is slowing but remains resilient. Payroll growth of just 64,000 in November, combined with downward revisions to previous months, reinforced concerns that the US economy is losing momentum without tipping into outright weakness.

At the same time, inflation has yet to cool enough to justify swift easing. This policy stalemate has kept markets guessing. Fed Governor Christopher Waller recently indicated that borrowing costs could be lowered by up to one percentage point if the labour market softens further, encouraging traders to factor in two rate cuts in 2026. Falling rate expectations typically weigh on real yields, a dynamic that tends to favour gold and silver.

Supply-side pressures are reinforcing the move. Silver is on track for its fifth consecutive annual deficit, as demand from solar energy, electric vehicles, and data infrastructure continues to expand. With inventories already tight, prices have become increasingly sensitive to even small shifts in investment demand.

Why it matters

The renewed rally is significant because it highlights a broader shift in how investors assess risk. Rather than positioning for a clear-cut growth or recession outcome, markets are preparing for an extended period of economic imbalance, where inflation, rates, and growth send conflicting signals. In such conditions, metals often reclaim their role as long-term stores of value rather than short-term trades.

Platinum’s advance is particularly instructive. Long overshadowed by gold and silver, the metal is now benefitting from persistent supply constraints. The World Platinum Investment Council expects another sizable market deficit in 2025, marking the third consecutive year where supply fails to meet demand.

As one analyst put it, “low elasticity in recycling, limited reinvestment at the mine level, and ongoing production challenges are making future supply risks increasingly difficult to dismiss.” That backdrop supports the view that platinum’s move reflects a structural re-pricing rather than a fleeting surge.

Impact on markets and investors

For investors, the metals rally is altering the dynamics of their portfolios. Gold continues to serve as a defensive cornerstone, underpinned by sustained central bank buying and geopolitical uncertainty. Silver, by contrast, has evolved into a hybrid asset, balancing its safe-haven appeal with expectations that industrial demand will remain firm even as global growth slows.

Platinum adds further complexity. South Africa, which produces roughly 70–80% of the global supply, has faced repeated mining disruptions that have constrained output. Meanwhile, exports to China have remained strong, and the launch of platinum futures on the Guangzhou Futures Exchange has bolstered confidence in future demand from Asia.

Physical markets are also showing signs of strain. Reports suggest that metal inventories are being relocated to the United States as firms hedge against potential trade disruptions, while liquidity in the London market has tightened. Together, these developments underscore how geopolitical risk and supply security are increasingly influencing commodity pricing.

Expert outlook

Looking beyond short-term data releases, Deriv expert Vince Stanzione believes the longer-term outlook for precious metals remains constructive as markets move into 2026. He points to the exceptional performance of 2025, when gold rose by around 60% to roughly $4,200 per ounce, and silver gained close to 80%, driven by concerns about inflation and strong industrial demand.

While he does not expect a repeat of those outsized returns, Stanzione still sees scope for further gains. He forecasts gold rising by 20–25% and silver by 25–30% in 2026, outpacing equity markets, where returns are expected to remain muted as valuations look increasingly stretched. He cautions that volatility and sharp pullbacks are likely, but maintains that the broader trend remains positive.

Central bank behaviour remains a cornerstone of the bullish case. Stanzione notes that official institutions added more than 1,000 tonnes of gold to reserves in 2025, led by the People’s Bank of China and the Reserve Bank of India. He expects continued buying in 2026 as diversification away from the US dollar gathers pace, following China’s extended accumulation streak since late 2022.

Silver’s outlook is further supported by its dual role as both a monetary hedge and an industrial input, with demand from solar energy and electric vehicles projected to exceed mined supply. Stanzione also highlights mining equities as a complementary angle, noting that valuations remain relatively restrained despite strong recent performance.

Historically, movements in gold prices have tended to translate into outsized changes in miners’ earnings, although factors such as currency strength and shifts in Chinese demand remain key risks to monitor.

Monthly price chart of Newmont Corporation (NEM) from 1997 to November 2025

On platinum and palladium, Stanzione remains cautiously optimistic. Both metals delivered solid gains in 2025 and continue to benefit from industrial applications, particularly in catalytic converters. While their markets are smaller and more volatile than gold and silver, they remain potential catch-up candidates if supply constraints persist.

Key takeaway

Metals are rising again as investors adjust to a landscape defined by unclear monetary policy and uneven economic signals. Record silver prices and platinum’s renewed strength point to tightening supply and a revival of defensive positioning. With inflation data and Fed guidance still pulling markets in different directions, precious metals continue to act as both a hedge and a signal. Near-term volatility may persist, but the underlying trend remains firmly supported.

Silver technical insights

Silver continues to trade within a strong upward trend, with prices holding near the upper Bollinger Band, indicating sustained bullish momentum. At the same time, the Relative Strength Index has moved deep into overbought territory, increasing the likelihood of consolidation or short-term profit-taking.

Initial support sits around $50.00, followed by $46.93. A break below these levels could trigger a deeper corrective phase. As long as prices remain above $50, however, the broader bullish structure remains intact, even if gains slow in the absence of a pullback.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.

FAQs

Why are metals rising again now?

Why is silver outperforming gold?

What is driving platinum’s breakout?

How do interest rate expectations affect metals?

Could the metals rally reverse?