Contents

Article

Could the Fed cut rates faster in 2026 than markets expect?

January 9, 2026

Article

Could the Fed cut rates faster in 2026 than markets expect?

January 9, 2026

Article

Could the Fed cut rates faster in 2026 than markets expect?

January 9, 2026

Will the Federal Reserve move more quickly on interest rate cuts in 2026 than markets currently anticipate? According to analysts, the possibility is growing as divisions within the central bank become more visible. While official forecasts continue to point to a measured pace of easing, some policymakers believe inflation has cooled sufficiently to justify a more decisive shift.

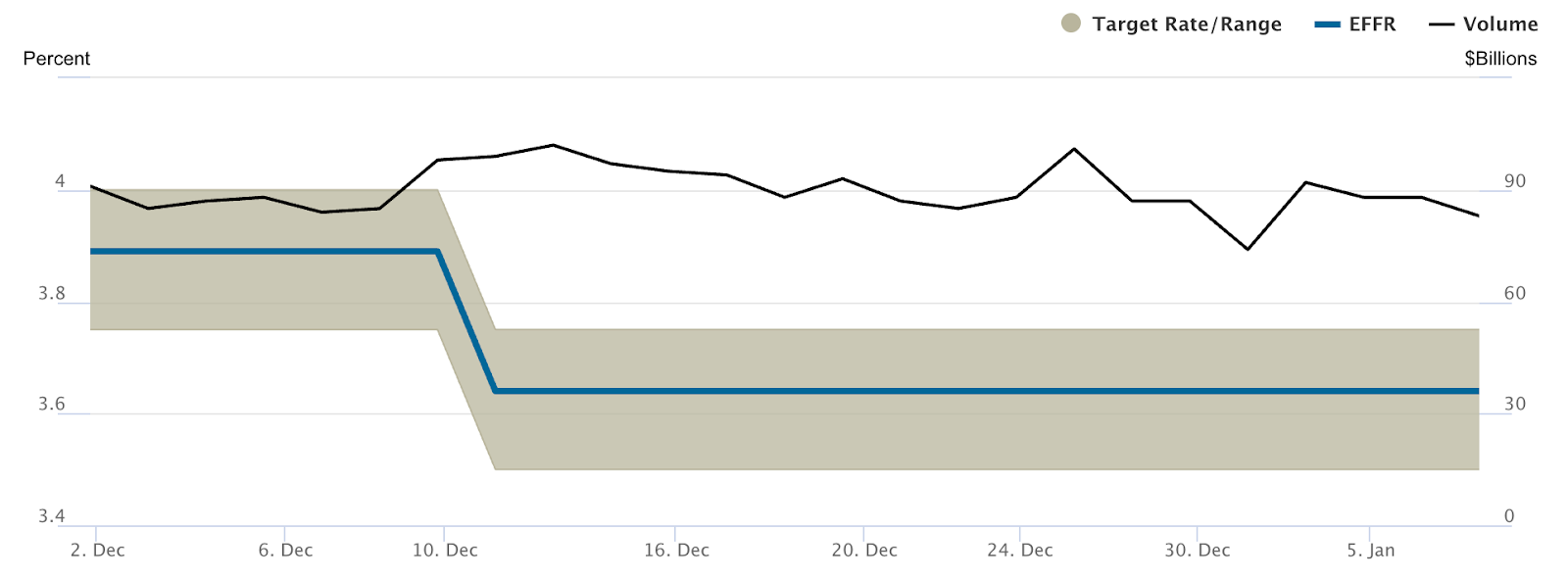

With the Federal Funds Rate holding in a 3.50%–3.75% range, the debate has turned to whether policy remains too restrictive for an economy showing signs of slower momentum. The balance between guarding against renewed inflation and supporting growth is now firmly at the centre of the Fed’s policy dilemma.

That tension sharpened after Fed Governor Stephen Miran called for as much as 150 basis points of rate cuts this year. His position stands well apart from current market pricing and from colleagues urging restraint. As labour market indicators soften and inflation edges closer to target, investors are increasingly alert to the risk that the Fed may ultimately pivot faster than it currently suggests.

What’s driving the Fed’s rate cut debate?

At the heart of the disagreement is how policymakers interpret recent progress on inflation and employment. Miran has argued that underlying inflation is hovering around 2.3%, close enough to the Fed’s target to allow for meaningful rate reductions without reigniting price pressures. In his view, maintaining elevated rates is weighing unnecessarily on hiring and labour participation.

Others within the Fed remain cautious. Several regional bank presidents prefer to wait for clearer post-shutdown data before adjusting policy further. They point to past cycles where inflation proved stubborn, warning that easing too soon could reverse hard-won gains if demand rebounds faster than expected.

Political dynamics have also intensified the debate. Miran’s temporary appointment by President Donald Trump has placed additional attention on the Fed’s decisions, particularly as concerns over recession and stagflation resurface. Although the central bank’s independence remains intact, the spotlight reflects how sensitive interest rate policy has become as growth slows.

Why it matters

This divide matters because markets respond to expectations as much as to actions. Shifts in tone from Fed officials can quickly ripple through bonds, equities, and currencies, even without an immediate policy change. When those signals conflict, uncertainty tends to rise, feeding volatility across asset classes.

Some economists argue that excessive caution carries its own risks. Analysts at Bloomberg Economics have highlighted that tight monetary policy affects employment with a delay, meaning today’s labour weakness may stem from earlier rate decisions. If the Fed waits too long, it may be forced into sharper cuts later, increasing the risk of market disruption.

Impact on markets and consumers

For households, the pace of rate cuts has direct financial consequences. Borrowing costs on credit cards, car loans, and home-equity borrowing remain closely linked to short-term rates, keeping pressure on household budgets despite easing inflation. A quicker easing cycle would gradually ease that burden, particularly for borrowers exposed to variable rates.

Markets have already begun to reflect the uncertainty. Bond yields are reacting more strongly to labour data, while equity valuations increasingly depend on whether growth can hold without further policy support. A faster-than-expected easing path would likely weigh on the US dollar, lift risk assets, and steepen the yield curve, signalling confidence in a controlled slowdown.

If the more hawkish voices prevail, tighter conditions may linger. That scenario would favour defensive positioning and could keep volatility elevated as investors recalibrate expectations around a slower-moving Fed.

Expert outlook

Current Federal Reserve projections still point to only one rate cut in 2026, underscoring the gap between official guidance and Miran’s more aggressive stance. The latest rotation of voting members on the Federal Open Market Committee also leans hawkish, reducing the likelihood of swift policy shifts in the early part of the year.

That said, analysts agree that incoming data will ultimately dictate the outcome. Measures such as jobless claims, wage growth, and labour force participation are likely to carry greater weight than headline inflation alone. A sharper deterioration in employment without renewed price pressures would strengthen the case for faster easing.

For now, the division within the Fed reflects uncertainty rather than institutional strain. Policymakers are navigating how a post-pandemic economy responds to prolonged restraint, and that challenge is likely to shape monetary policy decisions throughout 2026.

Key takeaway

The Federal Reserve heads into 2026 torn between caution and urgency. While official projections still favour gradual easing, calls for deeper cuts point to rising concern over labour market weakness. If employment data continues to soften without sparking inflation, the Fed may be forced to act more quickly than markets expect. For investors, labour indicators may prove the clearest signal of how fast policy ultimately shifts.

Disclaimer:

The performance figures quoted refer to the past, and past performance is not a guarantee of future performance or a reliable guide to future performance.

FAQs

Why is Stephen Miran calling for aggressive rate cuts?

Why are other Fed officials more cautious?

What does a ‘neutral’ interest rate mean?

How would faster rate cuts affect households?

Will markets force the Fed’s hand?